AI GPU Platforms Account for 90% of SMCI's Income: Is There More Growth Potential?

Super Micro Computer: Leading the AI Infrastructure Market

Super Micro Computer (SMCI) has rapidly evolved from a server manufacturer into a comprehensive provider of AI infrastructure, driven by soaring demand from AI data centers, hyperscale clients, AI-focused manufacturing, and enterprise customers. Today, 90% of SMCI’s revenue is generated by its AI GPU platforms. The company’s rack-scale AI clusters and integrated data center solutions have positioned it as a full-stack supplier in the AI ecosystem.

SMCI incorporates the latest AI chips from NVIDIA and Advanced Micro Devices (AMD) into its offerings, making it a preferred partner for organizations seeking cutting-edge performance. Recent product launches include advanced computing systems for AI factories, enterprise data centers, and edge AI, featuring NVIDIA RTX PRO Blackwell GPUs, as well as NVIDIA Hopper and AMD MI series GPUs.

In the second quarter of fiscal 2026, SMCI reported $10.7 billion in revenue from its OEM appliance and large data center division, accounting for roughly 84% of total sales. This success is attributed to SMCI’s ability to deliver end-to-end solutions, including computing, cooling, power infrastructure, networking, and management software.

SMCI’s comprehensive approach has established it as a one-stop solution for AI infrastructure, positioning the company to potentially achieve its $40 billion revenue target for fiscal 2026. However, SMCI does face some challenges in the near term.

One concern is its reliance on a small number of major clients, with a single customer contributing 63% of revenue in the second quarter of fiscal 2026. Additionally, potential scrutiny from U.S. export-control authorities has raised questions. Operating in a capital-intensive industry, SMCI’s inventory also increased to $10.6 billion during the same period.

Comparing SMCI with Industry Rivals

In the AI and data center sector, Super Micro Computer competes with Dell Technologies (DELL) and Hewlett Packard Enterprise (HPE).

Dell Technologies is a leading provider of servers and storage solutions, serving a wide range of enterprise and cloud customers. Its extensive distribution network and service capabilities give it an advantage in securing large contracts. While Dell’s growth in AI-specific systems has lagged behind SMCI, its ability to bundle hardware with services makes it a formidable competitor.

Hewlett Packard Enterprise is also making significant strides in AI and high-performance computing. Its GreenLake platform offers flexible, cloud-like consumption models that appeal to enterprise clients. HPE’s emphasis on hybrid cloud and AI workloads puts it in direct competition with SMCI, especially as SMCI pursues growth through its DCBBS strategy.

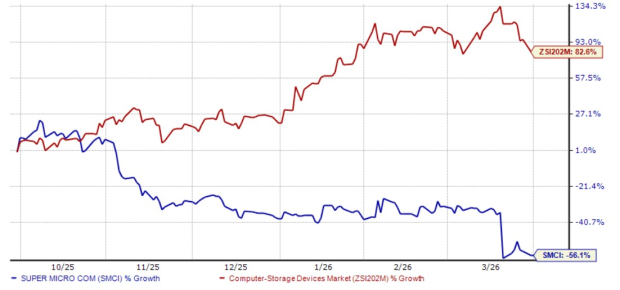

SMCI’s Stock Performance, Valuation, and Outlook

Over the past six months, shares of Super Micro Computer have declined by 56.1%, while the Zacks Computer – Storage Devices industry has surged by 82.6%.

SMCI Six-Month Performance Chart

From a valuation perspective, SMCI is trading at a forward price-to-sales ratio of 0.28, which is significantly below the industry average of 2.02.

SMCI Forward 12-Month (P/S) Valuation Chart

Consensus estimates from Zacks suggest that SMCI’s earnings for fiscal 2026 and 2027 are expected to grow by approximately 8.25% and 31%, respectively, with no changes to these forecasts over the past month.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitget Spot Margin Announcement on Suspension of SUEPR/USDT, DRIFT/USDT Margin Trading Services

Bitget to suspend stock token trading on Good Friday (April 3, 2026)

Mezo (MEZO) to be listed on Bitget Launchpool — lock BGB and MEZO to share 4,000,000 MEZO

Bitget PoolX to list Mezo (MEZO): Lock BTC to share 1,500,000 MEZO