PFE Shares Remain Above 200 & 50-Day Moving Averages for 3 Months: Strategies to Consider

Pfizer Stock Maintains Momentum Above Key Moving Averages

Since the start of January, Pfizer’s shares have consistently remained above both their 50-day and 200-day simple moving averages, reflecting ongoing investor optimism. The stock has climbed approximately 12.8% in 2026 to date.

Image Source: Zacks Investment Research

Signs of Recovery After COVID-Related Declines

Following several challenging years marked by a sharp drop in COVID product sales, Pfizer is beginning to show signs of a turnaround. This improvement is fueled by stronger-than-anticipated quarterly earnings, ongoing cost reduction strategies, successful product developments, and recent mergers and acquisitions. Despite these positive factors, Pfizer’s outlook for 2026 fell short of market expectations, and the company still faces significant hurdles, such as looming patent expirations.

Assessing Pfizer: Strengths and Weaknesses

The stock’s volatility has left many investors uncertain about their next move. To make informed decisions, it’s essential to review Pfizer’s core advantages and challenges.

Leadership in Oncology

Pfizer stands as a leading force in cancer treatment, a position further solidified by its acquisition of Seagen in 2023. Oncology now accounts for roughly 27% of Pfizer’s total revenue. In 2025, oncology sales increased by 8%, with key contributions from drugs such as Xtandi, Lorbrena, the Braftovi-Mektovi combination, and Padcev. The company has also expanded into oncology biosimilars, marketing six products that generated $1.3 billion in 2025—a 26% year-over-year increase. Pfizer’s late-stage oncology pipeline continues to grow, and by 2030, the company anticipates having at least eight blockbuster cancer therapies.

Growth Driven by New and Acquired Products

Pfizer’s reliance on COVID-related products has lessened, with operational revenue from non-COVID products rising thanks to established drugs like Vyndaqel, Padcev, and Eliquis, as well as new launches and recent acquisitions such as Nurtec and Seagen’s portfolio. In 2025, non-COVID product revenue grew by 6%, while newly launched and acquired products brought in $10.2 billion—a 14% operational increase over the previous year. Pfizer expects these products to continue delivering double-digit growth in 2026.

The company is actively rebuilding its pipeline through strategic acquisitions, including Seagen, Metsera, and Biohaven. In 2025, Pfizer invested about $9 billion in mergers and licensing deals, notably acquiring Metsera and entering a partnership with 3SBio. The addition of Metsera has reintroduced Pfizer to the obesity treatment market, following the discontinuation of danuglipron earlier in 2025. Metsera’s four innovative clinical programs are projected to generate substantial future sales. However, Pfizer still trails behind industry leaders Eli Lilly and Novo Nordisk in the obesity sector.

In 2026, Pfizer plans to initiate 20 pivotal clinical trials, including 10 focused on ultra-long-acting obesity candidates from Metsera and four for PF-08634404, a dual PD-1/VEGF inhibitor licensed from 3SBio.

With a robust pipeline and a suite of new products, Pfizer aims to restore revenue growth by the end of the decade.

2026 Financial Guidance Disappoints

Pfizer’s projections for 2026 suggest flat or slightly negative growth, which has dampened investor sentiment. The company anticipates total revenue between $59.5 billion and $62.5 billion, a decrease from $62.6 billion in 2025, mainly due to declining COVID product sales and the impact of upcoming patent expirations. Adjusted earnings per share are expected to fall to $2.80–$3.00, down from $3.22 in 2025, reflecting dilution from recent deals, lower COVID revenues, and increased taxes.

COVID Product Sales Continue to Decline

As the pandemic subsides, sales of Pfizer’s COVID treatments, Comirnaty and Paxlovid, have dropped sharply—from $56.7 billion in 2022 to $11 billion in 2024 and $6.7 billion in 2025. Comirnaty’s sales fell in 2025 due to limited vaccine recommendations in the U.S., while demand for Paxlovid decreased as infection rates declined. For 2026, Pfizer expects COVID-related revenue to fall further to around $5 billion.

Additional Challenges Ahead

Between 2026 and 2030, Pfizer faces significant revenue pressure from the loss of exclusivity on several major drugs, including Eliquis, Vyndaqel, Ibrance, Xeljanz, and Xtandi. This “patent cliff” is projected to reduce sales by about $1.5 billion in 2026. In addition, changes to Medicare Part D under the Inflation Reduction Act negatively impacted revenue in 2025, particularly for higher-priced medications, and this trend is expected to persist in 2026.

Stock Performance, Valuation, and Analyst Estimates

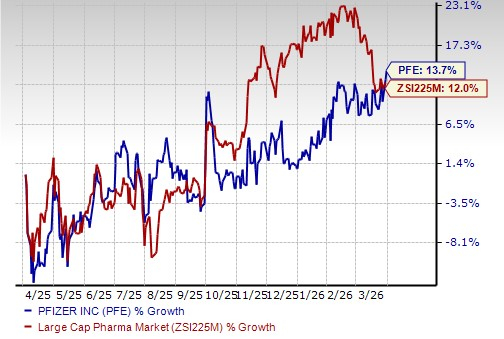

Over the past year, Pfizer’s stock has gained 13.7%, outpacing the large-cap pharmaceutical industry’s 12% increase.

Pfizer Outperforms Industry Peers

Image Source: Zacks Investment Research

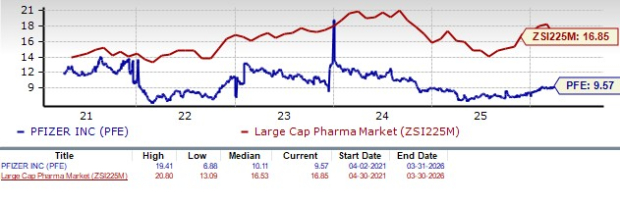

From a valuation perspective, Pfizer appears attractively priced compared to its peers, trading below its five-year average. The forward price-to-earnings ratio stands at 9.57, well below the industry average of 16.85 and Pfizer’s own five-year mean of 10.11. The stock is also less expensive than other major pharmaceutical companies such as AbbVie, Novo Nordisk, Eli Lilly, AstraZeneca, and Johnson & Johnson.

Current Valuation Snapshot

Image Source: Zacks Investment Research

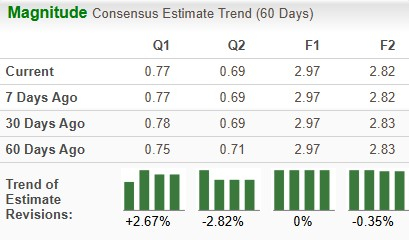

The Zacks Consensus Estimate for Pfizer’s 2026 earnings remains steady at $2.97 per share. The estimate for 2027 has edged down slightly over the past two months, from $2.83 to $2.82 per share.

Analyst Estimate Trends

Image Source: Zacks Investment Research

Should You Hold Pfizer Stock?

Pfizer is navigating a period of significant transition, facing near-term obstacles such as shrinking COVID sales, upcoming patent expirations, and regulatory headwinds from U.S. Medicare changes. While new and acquired products are contributing to growth, they have not yet fully offset the revenue lost from legacy and COVID-related products.

The company’s cautious outlook has led to negative sentiment among short-term investors, who may prefer to avoid the stock for now. However, long-term investors might consider holding Pfizer, which currently carries a Zacks Rank #3 (Hold), as the company invests in rebuilding its pipeline in oncology and obesity—areas expected to drive growth from 2028 onward. Pfizer’s ongoing cost-cutting and efforts to boost R&D productivity are also supporting profitability. The stock offers an attractive dividend yield of around 6.2%.

For the original article, visit Zacks Investment Research.

Zacks Investment Research

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

SOL Faces Influx of Exchange Deposits and Security Incident, Market Prospects Remain Unclear

Smart investors increase holdings in Japan ETFs as global tensions challenge ongoing reform efforts

General Motors Sees 9.7% Decline in Q1 Sales Due to Tariff Surge and Severe Winter Weather

uniQure Approaches April 13 Court Deadline Amid Stricter FDA Position on Gene Therapy Study