Here’s why investing in NeuroPace shares could be a smart addition to your portfolio at this time

NeuroPace, Inc.: Growth Prospects and Challenges

NeuroPace, Inc. is poised for continued expansion, fueled by robust adoption of its RNS technology, a growing network of referrals, and the integration of AI solutions that improve operational efficiency and device utilization. The company’s pursuit of an indication for idiopathic generalized epilepsy (IGE) represents a significant long-term opportunity. However, short-term profitability may be impacted by increased spending and seasonal trends, while the timeline for IGE-related revenue remains uncertain due to regulatory, reimbursement, and physician adoption hurdles. As a result, the company’s core business will remain the primary growth driver in the near term.

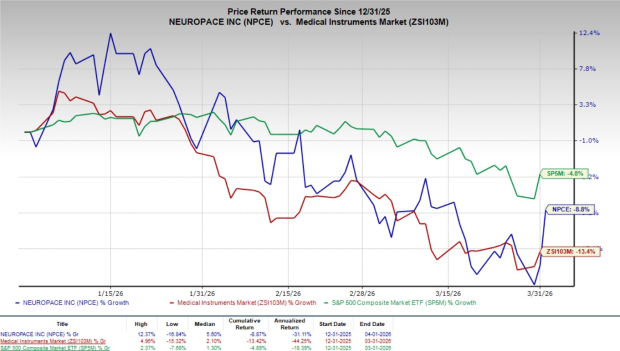

So far this year, shares of this Zacks Rank #2 (Buy) company have declined by 8.8%, outperforming the medical instruments industry, which fell 13.4%, and the S&P 500 Composite, which dropped 4.8%.

NeuroPace specializes in neuromodulation devices for epilepsy, with its flagship product being the RNS System—a closed-loop, brain-responsive implant that continuously monitors intracranial EEG, detects abnormal electrical activity unique to each patient, and delivers targeted stimulation to help prevent seizures. The company’s market capitalization stands at $442.7 million.

Looking ahead, NeuroPace forecasts an 82.3% growth rate by 2027 and expects to maintain strong momentum. Over the past four quarters, the company exceeded the Zacks Consensus Estimate for earnings three times and missed once, averaging a 24.7% positive surprise.

Image Source: Zacks Investment Research

Main Drivers of NeuroPace’s Expansion

RNS System Fuels Ongoing Growth

NeuroPace has reinforced its leadership in epilepsy care through the successful execution of its RNS (Responsive Neurostimulation) business. In 2025, the company achieved a 25% increase in revenue, with fourth-quarter sales up 24% year-over-year, largely due to a 26% rise in RNS System shipments. Management highlighted record numbers in prescribers, accounts, and patient pipeline, especially within Level 4 epilepsy centers, indicating strong market uptake and utilization.

Further growth is supported by the expansion of community referral channels and improved patient management, which streamlines the process from patient identification to device implantation. The company anticipates 20%-22% growth in its core RNS business for 2026 and remains confident in sustaining at least 20% annual growth within the adult focal epilepsy segment. Ongoing investments in salesforce expansion, incentive programs, and nurse navigators are expected to boost procedural volumes and drive consistent revenue growth as the company scales its commercial operations.

Expanding Indications to Reach New Patient Populations

A significant growth catalyst for NeuroPace is the potential approval of the RNS System for idiopathic generalized epilepsy (IGE), a largely underserved group. The company submitted a PMA supplement in December 2025, backed by positive NAUTILUS trial data showing a 77% median reduction in seizure frequency and a strong safety profile. The FDA has accepted the application and begun a 180-day review, aided by Breakthrough Device Designation. While 2026 guidance does not include IGE-related revenue, management sees this as a transformative opportunity. If approved, the company can leverage its existing clinical infrastructure and physician relationships for rapid adoption, opening a significant new market and strengthening its position in personalized neuromodulation.

AI Innovations and Product Pipeline Support Adoption

NeuroPace is advancing a range of AI-powered tools and platform enhancements to streamline physician workflows, boost efficiency, and maximize the value of its extensive intracranial EEG data. The Seizure ID tool, currently under FDA review and expected to launch in the first half of 2026, aims to quickly analyze patient data, detect seizures, and reduce clinician review time. The company is also developing remote care features, enabling therapy adjustments during telehealth visits and expanding access. Transitioning to a cloud-based clinician platform will allow for faster software deployment and scalability. Additionally, the development of a foundational AI model, built on over 24 million EEG recordings, is expected to optimize personalized treatments and improve patient outcomes. Collectively, these innovations are designed to increase system usage, enhance clinician productivity, and establish a scalable, data-driven neuromodulation platform.

Potential Challenges for NeuroPace

Short-Term Profitability Pressures and Seasonal Trends

Despite strong revenue growth, NeuroPace is deliberately increasing investments in its commercial and R&D operations, which will likely impact near-term earnings. The company projects an adjusted EBITDA loss of $9 million to $10 million for 2026, reflecting these heightened investments. Operating expenses are expected to be front-loaded, with more than half incurred in the first half of the year due to expanded hiring, marketing, and nurse navigator initiatives.

Management also noted typical seasonality, with first-quarter 2026 revenues projected at $21 million to $22 million and slower growth in the first half before accelerating later in the year. The conclusion of the DIXI Medical partnership in December 2025 removes a previous revenue source, making year-over-year comparisons more challenging. These factors suggest weaker short-term profitability and operating metrics, despite strong 2025 performance and two consecutive quarters of positive adjusted EBITDA, which could affect investor sentiment in early 2026.

Delayed Monetization from IGE Approval and Coverage

NeuroPace’s IGE PMA supplement, submitted in December 2025 and currently under FDA review, is progressing with ongoing discussions and a planned mid-cycle meeting, but the timing of approval remains unclear. Although the NAUTILUS trial demonstrated significant clinical benefits—including a 77% median seizure reduction at 18 months and a favorable safety profile—the company is awaiting regulatory clearance. Even with approval, immediate revenue impact is unlikely, as NeuroPace will need to implement physician training, expand referral pathways, and educate the broader medical community before seeing substantial volume growth. Accordingly, the 2026 revenue forecast of $98-$100 million does not factor in any IGE-related sales. Therefore, even if approval comes by mid-2026, there will likely be a delay before meaningful revenue is realized, leaving the core RNS business as the primary growth engine in the interim.

NeuroPace, Inc. Stock Performance

For more details on NeuroPace’s stock performance, see the latest price chart and quote.

Analyst Estimate Trends

Analyst sentiment for NeuroPace has improved for 2026, with the Zacks Consensus Estimate for loss per share narrowing by $0.14 to $0.51 over the past two months. The consensus revenue estimate for 2026 stands at $98.8 million, representing a 1.2% decrease from the previous year’s reported figures.

Other Noteworthy Medical Stocks

- Phibro Animal Health: Currently rated Zacks Rank #1 (Strong Buy), Phibro reported Q2 fiscal 2026 adjusted EPS of $0.87, beating estimates by 27.1%. Revenues reached $373.9 million, exceeding expectations by 4.7%. The company’s projected long-term earnings growth rate is 21.5%, compared to the industry’s 12.4%. Over the last four quarters, Phibro consistently beat earnings estimates, with an average surprise of 20.1%.

- GE HealthCare Technologies: Holding a Zacks Rank #2, GEHC posted Q4 2025 adjusted EPS of $1.44, surpassing estimates by 0.7%, with revenues of $5.7 billion, up 1.9% over consensus. The company’s estimated long-term earnings growth rate is 9.1%, compared to the industry’s 12.4%. GEHC beat earnings estimates in each of the last four quarters, with an average surprise of 7.5%.

- Cardinal Health: Also rated Zacks Rank #2, Cardinal Health reported Q2 fiscal 2026 adjusted EPS of $2.63, topping estimates by 10%, with revenues of $65.6 billion, 0.9% above expectations. The company’s projected long-term earnings growth rate is 15%, compared to the industry’s 9.2%. Cardinal Health exceeded earnings estimates in the last four quarters, with an average surprise of 9.3%.

The Next Wave of AI Investing

While the first wave of AI has already created significant wealth, the most well-known stocks may not offer the largest gains going forward. Lesser-known AI companies addressing major global challenges could provide greater returns in the coming months and years.

Get the Latest Stock Recommendations

For up-to-date recommendations from Zacks Investment Research, you can download the report "7 Best Stocks for the Next 30 Days."

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

SOL Faces Influx of Exchange Deposits and Security Incident, Market Prospects Remain Unclear

Smart investors increase holdings in Japan ETFs as global tensions challenge ongoing reform efforts

General Motors Sees 9.7% Decline in Q1 Sales Due to Tariff Surge and Severe Winter Weather

uniQure Approaches April 13 Court Deadline Amid Stricter FDA Position on Gene Therapy Study