Should You Keep Astera Labs Shares After a 36% Decline This Year?

Astera Labs Stock Performance Overview

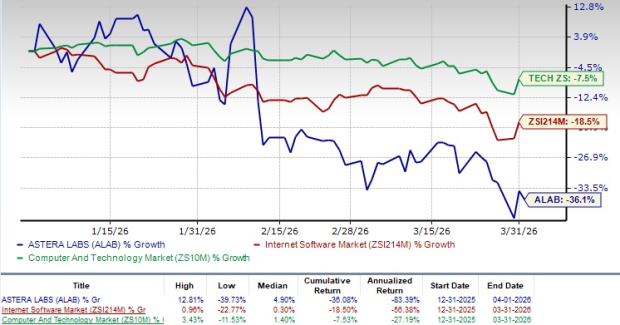

Astera Labs (ALAB) has seen its share price fall by 36.1% so far this year, a steeper drop compared to the broader Computer & Technology sector’s 7.5% decline and the Internet - Software industry’s 18.5% decrease. This significant underperformance is largely due to ongoing economic headwinds and intense competition within the PCIe retimers market.

Additionally, a shift toward a greater proportion of hardware sales has put pressure on ALAB’s profit margins. The company’s increased spending on research and development, along with recent acquisitions, has also weighed on its financial results.

Recent Stock Trends

Growth Drivers: Expanding Product Portfolio and AI Demand

Despite recent challenges, Astera Labs is leveraging its broad and innovative product lineup to meet the rising needs of AI infrastructure and connectivity. The company’s growing network of partners and strong demand for its PCIe solutions have been key contributors to its growth trajectory.

Strong Demand for PCIe Solutions Fuels Expansion

Astera Labs is rapidly enhancing its offerings to address the surging requirements of AI infrastructure and connectivity. Products such as Scorpio, Aries, and Taurus have played pivotal roles in this expansion.

The Aries PCIe 6 DSP retimer stands out as the only high-volume PCIe 6 DSP retimer currently available, with the Aries line achieving 70% year-over-year growth in 2025. This growth is driven by the increasing adoption of custom AI accelerators by major hyperscale data center operators. As the PCIe 6 upgrade cycle is still in its early stages, ALAB anticipates further momentum as more customers deploy PCIe 6-enabled AI accelerators and systems in 2026 and beyond.

The Scorpio P-Series has also been instrumental, accounting for over 15% of revenue in 2025. As the sole PCIe 6 fabric available at scale, Scorpio P-Series is expected to see continued growth in 2026, with shipments expanding to additional hyperscalers for next-generation AI platforms. The Scorpio X-Series is projected to enter high-volume production in the latter half of 2026, which should further boost revenue.

Astera Labs is well-positioned to capitalize on the AI connectivity market, which is forecasted to grow tenfold to $25 billion over the next five years. The Scorpio P-Series is ramping up, with shipments expected to reach more hyperscalers in 2026, while the Scorpio X-Series is set to begin high-volume production later that year, providing additional revenue opportunities.

Positive Q1 Outlook

Astera Labs anticipates robust demand for its Aries, Taurus, and Scorpio product lines, which are expected to drive growth in the first quarter of 2026.

- Projected Q1 2026 revenue: $286 million to $297 million

- Zacks Consensus Estimate for Q1 revenue: $292.5 million (an 83.45% increase year-over-year)

- Expected Q1 earnings: $0.53 to $0.54 per share

- Zacks Consensus Estimate for Q1 earnings: $0.54 per share (a 63.64% increase year-over-year)

Astera Labs, Inc. Price and Consensus

Competitive Landscape

Even with a growing product range and expanding partnerships, Astera Labs faces tough competition from industry leaders such as Marvell Technology (MRVL), Credo Technology (CRDO), and Cisco Systems (CSCO), all of whom are strengthening their positions in the AI infrastructure market.

- Marvell Technology introduced the Structera S 60260 in March 2026, the industry’s first 260-lane PCIe 6.0 switch, enabling higher-density and lower-latency scaling for AI data centers.

- Cisco Systems has integrated AI across its networking, security, collaboration, and observability products. In Q2 of fiscal 2026, Cisco reported $2.1 billion in AI infrastructure orders from hyperscalers and expects over $3 billion in AI infrastructure revenue from these customers for the year.

- Credo Technology announced in February 2026 that its 7nm Toucan PCIe retimer achieved PCI-SIG compliance for PCIe 5.0 speeds, ensuring compatibility, signal integrity, and low power consumption for next-generation AI and high-performance computing platforms.

Valuation: Trading at a Premium

Astera Labs’ shares are currently valued at a premium, as indicated by a Value Score of F. The company’s forward 12-month Price/Sales ratio stands at 12.58, which is significantly higher than the Computer & Technology sector’s average of 5.72.

Valuation Snapshot

Summary

Astera Labs’ solid fundamentals, expanding alliances, and increasing demand for AI solutions reinforce its leadership in connectivity technology. However, the company continues to face macroeconomic challenges, fierce competition, and concerns over its elevated valuation.

Currently, Astera Labs holds a Zacks Rank #3 (Hold), suggesting that investors may want to wait for a more attractive entry point.

Exploring Opportunities Beyond Nvidia

The AI sector has already created significant wealth, but the best-known stocks may not offer the highest returns going forward. Lesser-known AI companies addressing major global challenges could present more lucrative opportunities in the near future.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

SOL Faces Influx of Exchange Deposits and Security Incident, Market Prospects Remain Unclear

Smart investors increase holdings in Japan ETFs as global tensions challenge ongoing reform efforts

General Motors Sees 9.7% Decline in Q1 Sales Due to Tariff Surge and Severe Winter Weather

uniQure Approaches April 13 Court Deadline Amid Stricter FDA Position on Gene Therapy Study