Critical April: Is De-dollarization Coming Again?

Morning FX

It's already mid-April again. Around this time last year, the trade war was at its peak. The US dollar index was still surging at the beginning of last year, but soon plummeted, falling from 104 to 98 in April, marking the start of global de-dollarization.

Chart: The US Dollar Index’s “Dark April”

Although the war is not over, the market seems to be stirring again, anticipating post-war weakness in the US dollar. The war has shaken the US-led international order, giving the dollar’s credibility another blow.

I. Why Did the Dollar Index Drop Sharply Last April?

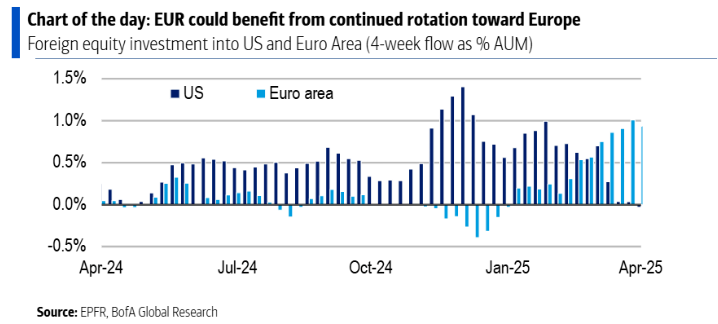

First is the reversal of the tit-for-tat tariff logic. When Trump displayed tariff rate charts at Mar-a-Lago, currencies of high-tariff countries all depreciated significantly, and fear in the market skyrocketed. However, tariffs proved to be just a bargaining tool, and as trade protectionism rose, capital inflows into the US during the Biden era started to reverse. Led by the euro, emerging market currencies followed closely behind.

Chart: European Capital Reflow

Second is the shaking of the Federal Reserve’s independence. In mid-April, Trump criticized Powell for cutting rates too slowly, threatening to replace the Fed chair. Rate cut expectations surged that year, with one-year SOFR swap rates dropping nearly 20 basis points in a single month. With monetary policy independence compromised, the market accelerated its selling of the dollar.

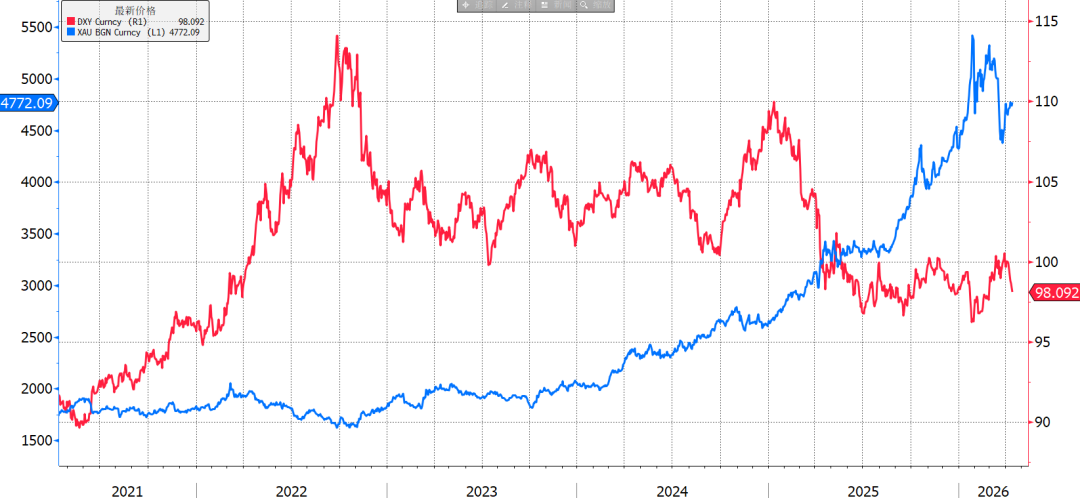

Third is the global shift in reserve asset allocation. The trade war intensified risk aversion, with gold breaking the $3,000 mark last April for the first time, entering a persistent upward trend. Central banks accelerated gold purchases as an alternative reserve to the dollar.

Chart: As Gold Rises, the Dollar Index Falls

II. Will the Same Scenario Play Out This Year?

Oil prices remain above $95, but the market seems indifferent to whether the US and Iran can reach any substantive agreements. The euro and Australian dollar have returned to pre-war levels, and the RMB has hit a new high for the year.

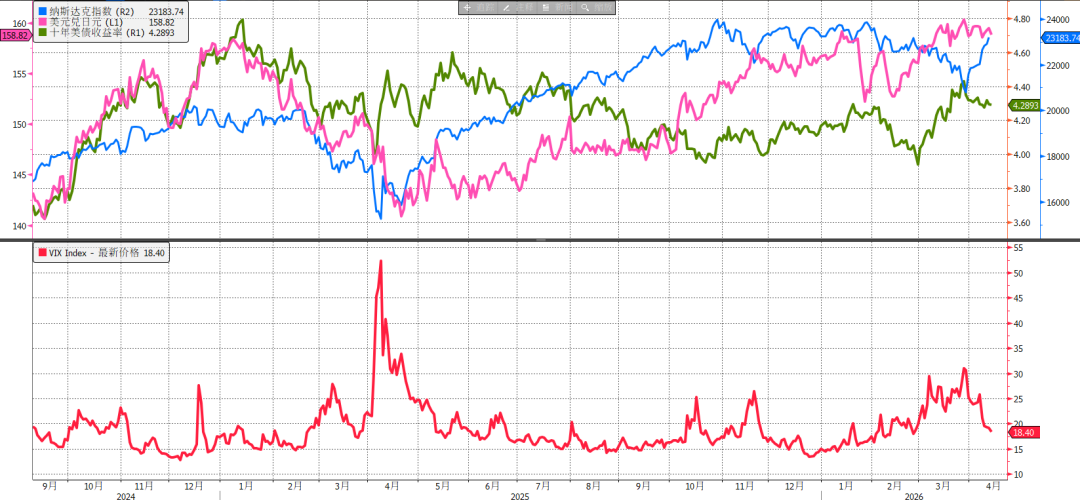

With each negative news event, the dollar index’s rebound is growing weaker, clearly indicating that the market is anxiously pricing in a second round of de-dollarization, and not just in the FX market. The reaction in equity markets has been even stronger: US stocks have recovered all losses, with the ChiNext index climbing above 3,500 points.

Chart: Risk Sentiment Has Returned to Pre-War Levels

Similar to last year, the war has again triggered a reallocation of capital. The support from high oil prices and risk aversion for the US dollar is very short-lived. If the war ends in a less-than-successful manner, the dollar's decline will likely continue. However, it should be noted that as economic data improves, the de-dollarization process in the second half of 2025 has almost stalled; further downside would require more negative catalysts.

III. Summary

(1) Last April’s scenario is playing out again. After the market has digested the impact of war, de-dollarization is making a comeback.

(2) However, the dollar’s decline will not necessarily be smooth. Currently, all assets have returned to pre-war positions, and early movers in the market will face even more intense competition.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

IAG (Iagon) 24-hour fluctuation of 45.1%: Trading volume surges over $12 million, triggering intense volatility

BAN (Comedian) fluctuates 40.1% in 24 hours: driven mainly by massive buying and technical breakthroughs

What to Expect in the Week Ahead (FOMC Rate Decision and Earnings from AAPL, GOOG, AMZN, META and MSFT)