Bitget UEX Daily | Nasdaq 10-Day Winning Streak Nearing Record; Semiconductor Stars Lead Surge to New Highs; ASML Earnings Release Today (April 15, 2026)

Bitget2026/04/15 01:34

Bitget2026/04/15 01:34

I. Key Headlines

Federal Reserve Developments

Fed Chair Nominee Kevin Warsh Hearing Scheduled for April 21

- President Trump’s nominee, former Fed Governor Kevin Warsh, has submitted his financial disclosure forms showing assets exceeding $100 million. The Senate Banking Committee’s top Republican has confirmed the hearing will take place next week on April 21, with a focus on price stability, inflation, and Fed independence.

- Treasury Secretary Bessent previously noted that the Fed’s inflation assessment has been off-target, with core inflation continuing to decline, suggesting that waiting for clearer data could require more aggressive rate cuts.

- Chicago Fed President Austan Goolsbee added that if the Iran conflict causes oil prices to remain elevated for a prolonged period and slows the return of inflation toward the Fed’s 2% target, the central bank might not cut rates until 2027. Market impact: Investors now have a clearer view of Fed policy continuity and potential easing paths, supporting improved pricing for risk assets.

International Commodities

Optimistic US-Iran Ceasefire Talks Weigh on Oil Prices

- On April 14, President Trump stated that the Iran war is “over.” The US and Iran have begun two weeks of negotiations, with follow-up talks planned in Pakistan. Vice President Vance described the situation as “optimistic.”

- Israel supports the ceasefire but excludes Lebanon; Saudi Arabia has resumed oil pipeline operations; Iran is considering suspending shipments through the Strait of Hormuz to facilitate dialogue. Market impact: Tail risks have dropped sharply and risk appetite has rebounded, directly driving significant declines in crude futures while boosting global equity risk assets.

Macroeconomic Policies

Treasury Secretary Bessent: Tariff Levels Likely to Be Restored by Early July

- Secretary Bessent said that after the Supreme Court ruled early tariffs unconstitutional, the administration will use Section 301 investigations and other authorities to rebuild the “tariff wall,” with restoration of previous levels possible as early as early July.

- He also stressed that the US economic fundamentals remain strong, projecting growth of over 3%—potentially reaching 3.5%—this year, with declining core inflation as a positive signal. Market impact: Near-term trade friction expectations have eased, but the long-term tariff rebuilding signal still warrants attention for its potential effects on corporate costs and supply chains.

II. Market Recap

Commodities & Forex Performance

- Spot Gold: After minor fluctuations, settled around $4,830/oz and remains in a high-level upward oscillation.

- Spot Silver: Moved in tandem with gold, holding steady above $79/oz, supported by solid industrial demand.

- WTI Crude: Fell to around $87/barrel; the optimistic US-Iran ceasefire talks directly reduced the energy risk premium.

- Brent Crude: Declined in parallel to around $95/barrel.

- US Dollar Index: Down about 0.03%, closing near 98.131; rising risk appetite has diminished the dollar’s safe-haven appeal.

Cryptocurrency Performance

- BTC: 24H gain of approximately 0.18%, trading around $74,500; 4-hour chart shows an oscillating uptrend.

- ETH: 24H decline of approximately 1.5%, trading around $2,335.

- Total Crypto Market Cap: 24H increase of approximately 0.2%, standing at roughly $2.6 trillion.

- Market Liquidations: 24H total liquidations of about $4.33 billion, with long positions liquidated at $2.0 billion and short positions at $2.3 billion; clearing was relatively balanced across leveraged positions.

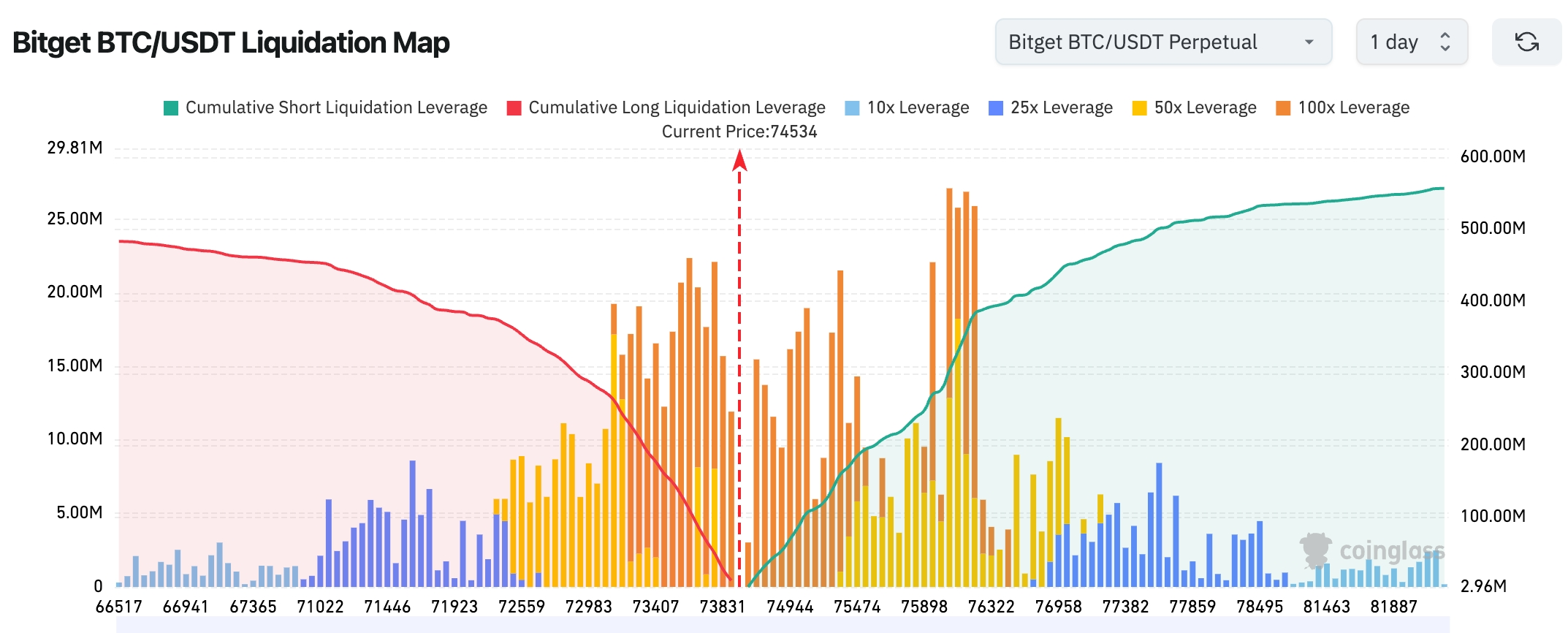

- Bitget BTC/USDT Liquidation Heatmap: Current price (≈$74,534) sits near the long-short liquidation boundary. Accumulated short-side liquidation pressure above is clearly larger, implying that any upward move could easily trigger cascading short squeezes. Below, dense long-side liquidation zones are concentrated between $73,000–$74,000; a break lower would likely spark a long-side stampede. Therefore, price action in the near term is prone to “pinching” volatility within this range.

- Spot ETF Net Flows: BTC spot ETFs recorded net inflows of approximately $152 million yesterday; ETH spot ETFs saw net inflows of about $3.3 million.

- BTC Spot Inflows/Outflows: Yesterday inflows totaled approximately $3.325 billion, outflows $3.427 billion, resulting in a net outflow of $29 million.

US Stock Index Performance

- Dow Jones: +0.66% at 48,535.99 points; continued rebound but with relatively modest gains.

- S&P 500: +1.18% at 6,967.38 points; now just one step away from its all-time closing high.

- Nasdaq: +1.96% at 23,639.08 points; extended its winning streak to ten consecutive sessions, driven primarily by technology and semiconductor sectors.

Tech Giants Performance

- Nvidia (NVDA): +3.78% ($196.51), catalyzed by the release of its quantum AI model.

- Alphabet-A (GOOGL): +3.61% ($332.91), supported by expectations for AI application rollout.

- Apple (AAPL): -0.14% ($258.83), minor pullback amid an overall positive tech-sector atmosphere.

- Microsoft (MSFT): +2.27% ($393.11), steady cloud and AI business performance.

- Amazon (AMZN): +3.81% ($249.02), synergy between e-commerce and cloud services.

- TSMC (TSM): +2.79%, benefiting from recovering semiconductor supply-chain demand.

- Broadcom (AVGO): +0.27%, confidence boosted by the Meta custom-chip partnership.

- Meta (META): +4.41% ($662.49), AI accelerator cooperation agreement secured.

- Tesla (TSLA): +3.34% ($364.20), riding broader tech-sector sentiment. Core driver: AI-themed trading has regained momentum, and easing geopolitical risks have further amplified valuation expansion across tech stocks.

Sector Movers Watch

Semiconductors & Optical Communications rose more than 3%

- Representative stocks: Coherent (COHR) hit a new high at $313.42; KLA Corporation (KLAC) reached a new high at $1,795; Lam Research (LRCX) hit a new high at $272.

- Driving factors: Strong AI data-center demand combined with Nvidia’s quantum AI model release has propelled the entire industry chain higher.

Quantum Computing Concepts surged more than 15%

- Representative stocks: SEALSQ +21.03%, IonQ +20.16%, D-Wave Quantum +15.84%.

- Driving factors: Nvidia’s launch of the world’s first open-source quantum AI model directly ignited market enthusiasm.

III. In-Depth Company Analysis

1. Nvidia – Market Cap Soars $7,615 Billion in 10 Days

Event Overview: After Tuesday’s close, Nvidia extended its daily winning streak to ten sessions—the longest since 2023—with a cumulative gain exceeding 18% over ten days, adding roughly $7,615 billion (approximately RMB 5.19 trillion) to its market capitalization. At the same time, the company officially released the world’s first open-source quantum artificial intelligence model, marking another leap forward in its AI-quantum computing intersection strategy. The open-source nature of the model is expected to accelerate industry ecosystem development and further solidify Nvidia’s absolute leadership in computing infrastructure. Market Interpretation: Institutions broadly expect the computing-power leader to maintain long-term monopoly advantages in the AI-quantum computing crossover space. They view this milestone as validation of the depth of its technological moat and a catalyst for explosive growth in AI training and inference demand over the coming years, reinforcing the valuation-expansion thesis amid easing geopolitical tensions and recovering risk appetite. Investment Insight: As the core infrastructure play in AI, Nvidia remains the strongest bellwether of the tech bull market. Investors may consider strategic accumulation on pullbacks, especially with quantum AI applications accelerating, where its long-term compound growth potential stays highly compelling.

2. Meta Platforms – Partnership with Broadcom to Build 1-Gigawatt Custom Chips

Event Overview: Meta Platforms and Broadcom announced a comprehensive agreement extending their collaboration on Meta’s self-developed AI accelerator designs and jointly advancing a 1-gigawatt custom-chip project to meet the massive computing needs of next-generation AI training and inference. The partnership reflects Meta’s strategic shift toward greater self-sufficiency in AI infrastructure and the broader industry trend of tech giants increasing in-house R&D to reduce reliance on external suppliers. Market Interpretation: Wall Street analysts see this as signaling a new phase in the AI capex cycle. Accelerating in-house chip development not only optimizes cost structures but also significantly improves order visibility across the upstream semiconductor supply chain. Multiple brokerages have raised Broadcom price targets, emphasizing that mega-platform AI spending from Meta and peers will be a key support for semiconductor demand. Investment Insight: The AI capital-expenditure cycle remains firmly in an uptrend. Self-developed investments by Meta and other giants will drive multi-link, long-term growth across the industry chain. Investors should closely track execution progress on similar cooperation projects to capture structural opportunities in the AI hardware ecosystem.

3. Broadcom (AVGO) – Expanded AI Custom-Chip Project with Meta

Event Overview: Under the comprehensive cooperation agreement with Meta Platforms, Broadcom will deepen collaboration on AI accelerator design and jointly push forward the 1-gigawatt custom-chip project aimed at delivering high-efficiency computing power for Meta’s next-generation AI training and inference. This represents one of Broadcom’s largest commercial deployments in the AI custom-chip space in recent years. Having already achieved rapid revenue growth through deep ties with hyperscalers, this expansion further underscores Broadcom’s pivotal position in the AI semiconductor supply chain. Market Interpretation: Analysts note that Broadcom, leveraging its technological edge in custom ASICs, is transitioning from a traditional semiconductor supplier to a core platform provider for AI infrastructure. Multiple brokerages believe the partnership not only enhances order certainty for Broadcom but also injects confidence into the entire AI-chip ecosystem. In an environment of easing geopolitical risks and recovering global capital expenditure, Broadcom’s growth visibility stands notably above the industry average. Investment Insight: As a leader in AI custom chips, Broadcom’s binding relationships with major platforms will continue to drive outsized earnings growth. Investors should treat it as a core holding within the semiconductor sector and focus on valuation re-rating opportunities tied to the pace of AI capex realization.

4. ASML – Today’s Earnings in Focus

Event Overview: As the global leader in semiconductor equipment, ASML will release its quarterly results today. The market is paying close attention to EUV lithography order trends and the latest guidance on AI-chip demand. Having already benefited from robust AI-driven demand for advanced-process equipment, this earnings report will serve as a key gauge of semiconductor-cycle recovery strength—particularly with geopolitical easing now reducing supply-chain uncertainty. Market Interpretation: Analysts widely anticipate strong orders that will further confirm the sustainability of AI capital expenditure. Several brokerages maintain Buy ratings and have raised price targets, arguing that ASML’s technological barriers in advanced-process equipment position it to fully capitalize on global chipmakers’ capacity-expansion wave. Reduced geopolitical risk also provides additional support for supply-chain stability. Investment Insight: Semiconductor-equipment prosperity directly mirrors AI capex intensity, and ASML remains the upstream core name in global chip manufacturing. Investors can use today’s results as a critical reference point for judging industry-cycle inflection and strategically position for long-term growth in the semiconductor-equipment segment.

IV. Cryptocurrency Project Updates

- Bloomberg ETF analyst James Seyffart disclosed on X that 21Shares has updated the filing for its Hyperliquid ETF, proposing the ticker THYP.

- Bitcoin briefly broke above the key $76,000 resistance overnight before retreating to around $74,000, failing to sustain a decisive breakout and continuing its two-month-plus sideways consolidation. K33 Research head Vetle Lunde noted that Bitcoin perpetual-contract funding rates have remained negative for 11 consecutive periods. Despite the recent price rebound, traders still lean bearish, indicating that market positioning remains short-biased even during rallies. Meanwhile, open interest continues to rise, suggesting new short positions are being added rather than closed.

- Goldman Sachs has filed for a Bitcoin Premium Income ETF. The fund aims to generate current income while retaining upside potential from Bitcoin price appreciation.

- Bitwise CIO Matt Hougan and Head of Research Ryan Rasmussen stated in their latest report that since the US-Israel airstrikes on Iran on February 28, Bitcoin has risen about 12%, while the S&P 500 fell roughly 1% and gold dropped about 10%. Bitwise attributes Bitcoin’s strength to global financial-system fragmentation and the “weaponization” of payment infrastructure rather than a contradiction with geopolitical risk. The firm positions Bitcoin as an asset betting simultaneously on “store of value” and “international settlement currency,” noting that Iran’s reported willingness to accept Bitcoin for certain oil-related payments elevates its settlement-currency optionality. They view $1 million as a possible baseline price—not an upper limit—in Bitcoin’s long-term valuation framework.

- Rakuten Wallet, the crypto platform under Japan’s Rakuten Group, announced the listing of XRP for spot trading and payment use. Users can exchange Rakuten points directly for XRP and spend it via Rakuten Cash/Pay in everyday Japanese consumption scenarios. The integration connects XRP to Rakuten’s ecosystem of approximately 44 million users, over 3 trillion accumulated points (roughly $23 billion), and more than 5 million merchants across e-commerce and payment networks.

V. Today’s Market Calendar

Data Release Schedule

| 08:30 | United States | New York Fed Empire State Manufacturing Index | ⭐⭐⭐ |

| 08:30 | United States | Import Price Index | ⭐⭐ |

| 10:00 | United States | NAHB Housing Market Index | ⭐⭐⭐ |

| 20:00 | United States | Multiple Fed Officials Speak | ⭐⭐⭐⭐ |

Key Events Preview

Wednesday, April 15

- ASML (ASML) to release Q1 results before the market open.

- The global semiconductor supply-chain price-increase wave is accelerating transmission from costs to the entire chain—watch for margin performance at related companies.

Thursday, April 16

- TSMC (TSMC) Q1 results before the open; Netflix (NFLX) Q1 results after the close ★★★★★

- US weekly initial jobless claims data for the week ending April 11.

- Fed officials to speak intensively; release of the Fed’s Beige Book. Any “hawkish” signals could weigh on risk appetite ★★★★★

Friday, April 17

- Earnings season continues, potentially including other regional banks or small/mid-cap tech names; markets may enter weekend caution mode.

- Overall weekly trading guidance: Earnings results and any Fed “hawkish” signals will dominate sentiment. Continue monitoring Iran developments and follow-up US-Iran talks. Focus on structural opportunities in banking, technology, energy, and semiconductor sectors.

Institutional Views

Prominent investment-bank strategists widely agree that the rapid easing of geopolitical tensions has become the strongest catalyst in current markets. The sharp reduction in tail risks has directly fueled a broad recovery in risk appetite. Morgan Stanley strategists point out that each positive development in US-Iran negotiations reinforces traders’ conviction that “war will not derail the economy,” combining with expectations of potential Fed easing to push the S&P 500 near all-time highs and extend the Nasdaq’s ten-day winning streak as a clear reflection of tech-valuation repair. Goldman Sachs emphasizes that falling oil prices and a weaker dollar are resonating positively for emerging markets and crypto assets. At the same time, AI-themed rotation across semiconductors, optical communications, and quantum computing is expected to persist. Institutions recommend overweighting growth-oriented tech and cyclically sensitive assets. In summary, near-term market sentiment is dominated by repair and recovery, yet investors should remain alert to possible reversals as negotiation details materialize.

Disclaimer: The above content is compiled by AI search and verified by humans for publication only; it does not constitute any investment advice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

ENSO (ENSO) fluctuated by 61.2% in 24 hours: trading volume surged over 100 times, triggering speculative pumping

SOMI (Somnia) fluctuates by 45.1% in 24 hours: Trading volume surge drives price rebound

ZBT (ZEROBASE) fluctuated 45.6% in 24 hours: Trading volume surged over 400%, causing intense volatility