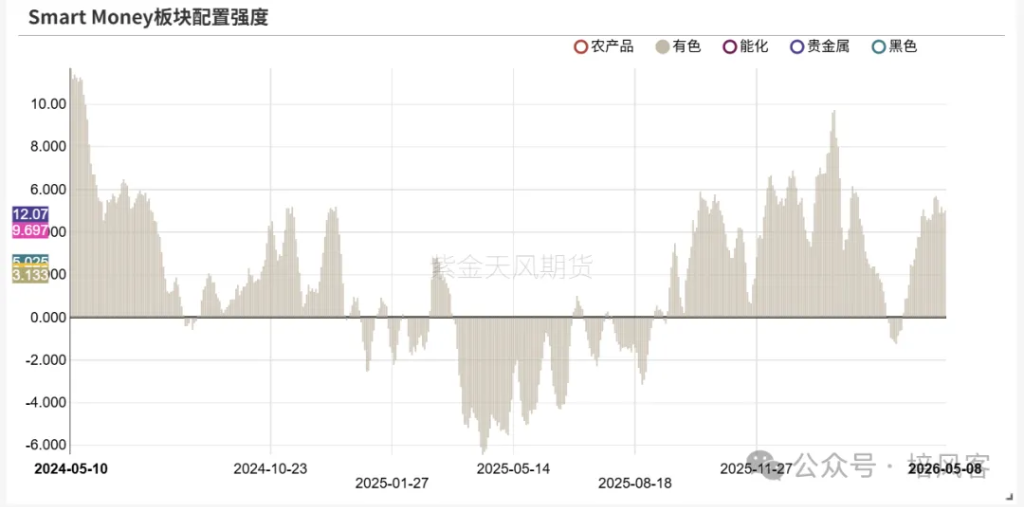

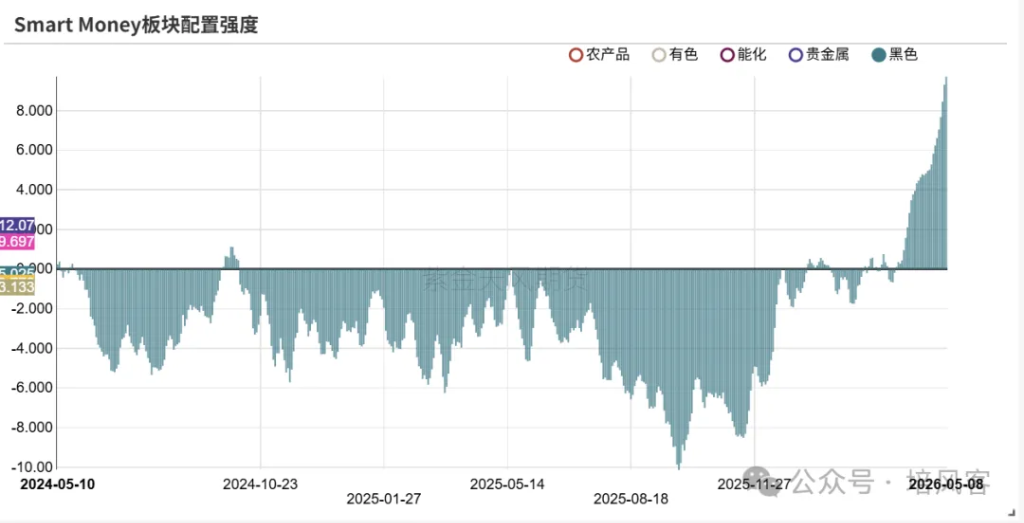

Differences are widening, the market is entering a "multi-narrative era"

Starting with metals, which I am more familiar with, I believe everyone may have sensed that, in the past period, differing opinions in the metals sector have become more common, while overall interest in the sector has also decreased. Of course, this also depends on what point in time you choose as the starting reference. For example, starting from the emotional low in March, the rebound triggered by the end of the war was very palpable, but here I am discussing a span of a year or so.

There is plenty of data to support these views, whether from the commodities market or the futures market.

In fact, this point has been repeatedly discussed in this public account since the end of last year. In my view, base metals, together with precious metals, outperformed most other commodities in the three-year commodity bear market from 2022 to 2025. It’s not surprising that precious metals performed well—this is the typical early-cycle story. Copper has its own structural narrative, which I have explained countless times and will not repeat. It's not surprising that, by 2026, the focus of commodities shifts to other varieties.

And if we narrow the overall perspective down to specific varieties, whether at the numerous discussion sessions in Hong Kong a few days ago or elsewhere among investors, we can hardly find a single variety with a very smooth bull market narrative.

Aluminum has short-term supply-demand conflicts, but also long-term expansion potential; discussion on nickel’s supply side even feels a bit like a Rashomon situation. Almost everyone agrees that, as long as the industrial trend does not change, the downside for copper is less than 10%, with upside potential still present. Yet, on the one hand, this is after all the start of the off-season, and on the other hand, it ties into the current hot topic of U.S. equities. The other varieties need not even be mentioned.

I believe this essentially comes down to two factors: a bull market narrative either requires supply-demand logic, or genuinely low prices. For example, at the end of 2023, the demand narrative for copper was not robust—most believed that copper prices typically fell during rate-cutting cycles and hadn't seen a turning point in traditional demand. However, with low inventories and prices not far above cost support, people felt buying on dips made sense. Alternatively, in 2024, precious metals saw capital inflows and central bank gold purchases during the rate cut cycle, even though there were divergences over the number of cuts, the logic stood firm.

Now, I feel that the K-shaped economy is fully understood by the market: varieties with strong demand are far from cost support, while those with weak demand are focused within traditional industries where no inflection point has been found. So, overall, my feeling is that there is a widespread mindset that:

- For varieties like copper, which have benefited from the AI narrative over the past two years and have significant supply-side pressures (trading far above cost support), people remain optimistic, but interest is noticeably lower than when copper was at the 75,000–80,000 range.

- For varieties like nickel, which previously struggled, supply-side events have brought prices closer to cost support, interest has increased quickly, but investors want a clearer supply-side logic.

Therefore, although copper and nickel have performed vastly differently over the past three years, both have seen choppy trends recently.

I have three conclusions on this part:

First, I don’t think the commodities bull market is over. I haven't seen a narrative where aggregate demand has peaked, nor have I seen China or the U.S. discuss suppressing economic development or meaningfully tightening fiscal or monetary policy. Nor do I see a major supply-side loosening. At least not in the short term.

Second, I don’t place all commodity interests within base metals. This was absolutely the right approach in the first half of this year, and I think the driving factors leading to this situation are still continuing, so this approach can continue as well.

Third, within base metals, I will not focus solely on copper. I think copper's risk-reward is not as good as other metals.

On the third point, I’d like to use nickel as an example. I’ve seen a lot lately in nickel that gives me a sense of déjà vu. For example, the downstream rejection of supply-side disruptions recently is similar to what happened earlier in chemicals, and in fact also to copper between 2023 and 2024. In the summer of 2024, when copper was being cornered, downstream buyers would only accept prices below 80,000, but today, you ask, and there are plenty willing to buy at 95,000. There are, of course, many reasons for this that don’t need elaboration. For example, now people are discussing the Indonesian government's view of nickel prices at 18,000–20,000 dollars. This topic itself is debatable, but also reminds me of a discussion about copper a few years ago. Back then, people said the price low set by extreme events in the summer of 2022 proved cost support was around 8,000 dollars; thus even in 2023 or 2024, when copper rose to 9,000 dollars, hedging interest would naturally decline over time.

Of course, these two varieties also have differences. Copper experienced a shift in downstream demand and inventory hoarding prompted by tariffs. Nickel’s downstream, such as stainless steel and batteries, still lacks a clear narrative. Moreover, supply-side issues in nickel are more policy-related than industry-based. Still, I think it’s a variety worth watching, because stainless steel (or the property chain), batteries, and Indonesian policy all carry significant uncertainty but also potential resonance upward. It requires study, but is worth studying.

Returning to the macro view, I think there are essentially only two key questions to answer right now.

The first question is whether there are macro risks. Currently, industry dynamics matter more than macro ones; at a detailed level, AI's influence on the market outweighs indicators like CPI and employment rate. On a larger scale, the competition between China and the U.S. is clearly about technology and warfare, not whose GDP grows faster. So, the impact of macro on the market, over the past two years, has shifted from being focused on macro narratives to watching for macro risks—only paying attention when risks are present.

Let me add a side note here—perhaps because I like macro, historically, macro often sends a bizarre narrative precisely when it doesn't seem important. In Q4 2019, everyone believed there wouldn’t be a rate cut in 2020, or in Q1 2025, when the "American exceptionalism" story encounters "Liberation Day," for instance.

The second is the basic assumption regarding the K-shaped divergence: can the outperformance of the AI sector over all other industries continue?

The answer to this, in my view, depends entirely on the depth of AI industry penetration. Supporters of K-shaped divergence believe this has always been the trajectory of human history—a technical breakthrough in one industry takes time to drive development in others. For example, it took several years from the start of the mobile internet in 2012 until the economic recovery in 2016-2017. Those opposed to this view also have plenty of data to support their argument.

My own view is the same as with metals—I prefer diversification, to pursue several types of technology instead of putting all my eggs in the AI basket. In reality, I believe all technology recognized by China and America’s industrial policies and capital markets is worth pursuing.

On whether there are macro risks, I do think there are, but they are the kind of risks you buy protection against, not the kind that justify a full bearish stance. I think this is best explained using Kevin Warsh’s framework.

Comprehensive bearish risks are ones where, say, one day you believe the Fed will hike rates—for example, like in 2022, when savvy investors saw the Fed chair emphasize controlling inflation and ignored the Fed’s own statements in March that it might hike to just 2%. Protection-type risks resemble 2019, when Powell said he’d agreed with the commercial banks on the desired reserve balance, only for reality to be different.

The former is intentional economic tightening, while the latter arises from actions gone awry. Right now, I think it’s more like the latter. There’s no doubt Kevin Warsh wants to bring change, and such changes are highly likely to cause volatility and risk. But does he have the power, in 2026, to persuade the American public to tolerate a rising unemployment rate and accept an economic downturn? I find that nearly impossible.

As for oil prices, private credit, overheated short-term sentiment, even the new virus—all these make sense as concerns but do not affect the overall conclusion.

To sum up, there are five main equity categories: financials, cyclicals, consumer, growth, and stability. I don’t think the China-U.S. competition will hinge on whether China Merchants Bank outperforms Wells Fargo, or whether our hydroelectric stations are more powerful. Thus, I don’t see stability and finance as the main theme.

A cyclical consumer turning point may be triggered by economic recovery or the CPI stabilizing and turning up; it's possible but has not yet appeared. In fact, consumer also has potential for a structural inflection point. Drawing from the Cold War as an example, if one day China and the U.S. both get weary, like in the 1970s, and put their swords away, shifting national resources from companies and government to individuals, then consumer might also see a structural opportunity—but I don't see that happening yet.

Growth and cyclicals are currently the areas I see with frequent industrial policies and more prominent opportunities, and also the focus of this article. I'm not as familiar with the technology sector, so I prefer a diversified approach; honestly, the China-U.S. technology race will unfold on several fronts. After exchanging views with friends in space and nuclear fusion, I believe these areas are also full of imagination, offering transformative technologies for humanity. In the resource sector, which I know well, people have clearly started exploring a wider array of varieties instead of focusing just on precious metals and copper.

Considering macro risks—now, with oil at 100, a new Fed chair coming in, and the midterms in the second half—I feel that diversification brings a bit of safety. Of course, there is a cost. If the AI sector continues to outperform alone, this means forgoing some returns. But for me, that's acceptable.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

NAORIS (NAORIS) fluctuates 45.0% in 24 hours: Futures trading volume surge and whale activity drive V-shaped rebound

TOWN (Alt.town) sees 234.1% fluctuation in 24 hours: Low liquidity trading amplifies price volatility

US (US) fluctuated 45.0% within 24 hours: Microstructure volatility in low liquidity markets