Bitget UEX Daily | Iran Rejects US Peace Proposal, Crude Oil Surges; AI Infrastructure Investment Surges, US Stocks Tech Hits New Highs (May 11, 2026)

Bitget2026/05/11 01:13

Bitget2026/05/11 01:13

1. Hot News

Fed Dynamics

Chicago Fed President Warns of AI Double-Edged Sword Effect

- Chicago Fed President Goolsbee told a Stanford conference that if AI productivity expectations materialize, interest rates will rise; if they do not, stagflation could follow.

- Businesses and households have front-loaded consumption and investment based on these expectations, potentially overheating the economy.

- Market Impact: Investors are reminded that the AI boom carries risks; the Fed’s policy path may diverge sharply depending on how technology actually unfolds, requiring caution in rate forecasts.

International Commodities

Saudi Aramco Q1 Profit Beats Expectations, Hormuz Disruption Risk Remains

- Saudi Aramco posted adjusted Q1 2026 net profit of $33.6 billion, up 26% year-over-year; its east-west pipeline running at full capacity has helped cushion global energy shocks.

- CEO Amin Nasser warned that any blockage of the Strait of Hormuz lasting more than a few weeks could extend supply disruptions into 2027.

- Market Impact: This heightens energy-supply uncertainty, intensifying short-term oil-price volatility while underscoring the importance of alternative transport routes.

2. Market Review

Commodities & FX Performance

- Spot Gold: $4,688/oz, -0.57%.

- Spot Silver: $80.2/oz, -0.12%.

- WTI Crude: $98.82/bbl, +3.56%, volatility intensified by potential Hormuz disruptions and reinforced by Saudi Aramco’s comments on supply concerns.

- Brent Crude: $104.6/bbl, +3.35%, moving in tandem with WTI as shipping-risk premium widens.

- US Dollar Index: 97.84, +0.15%, fluctuating modestly amid hawkish Fed rhetoric while AI-related uncertainty caps upside.

Cryptocurrency Performance

- BTC: +1.19% in 24H, currently around $88,168.2, continuing its oscillating uptrend.

- ETH: +1.41% in 24H, currently around $2,357.

- Total Crypto Market Cap: +1.9% in 24H, now approximately $2.93 trillion.

- Market Liquidations: $3.76 billion total in 24H, with short-side liquidations at $2.49 billion.

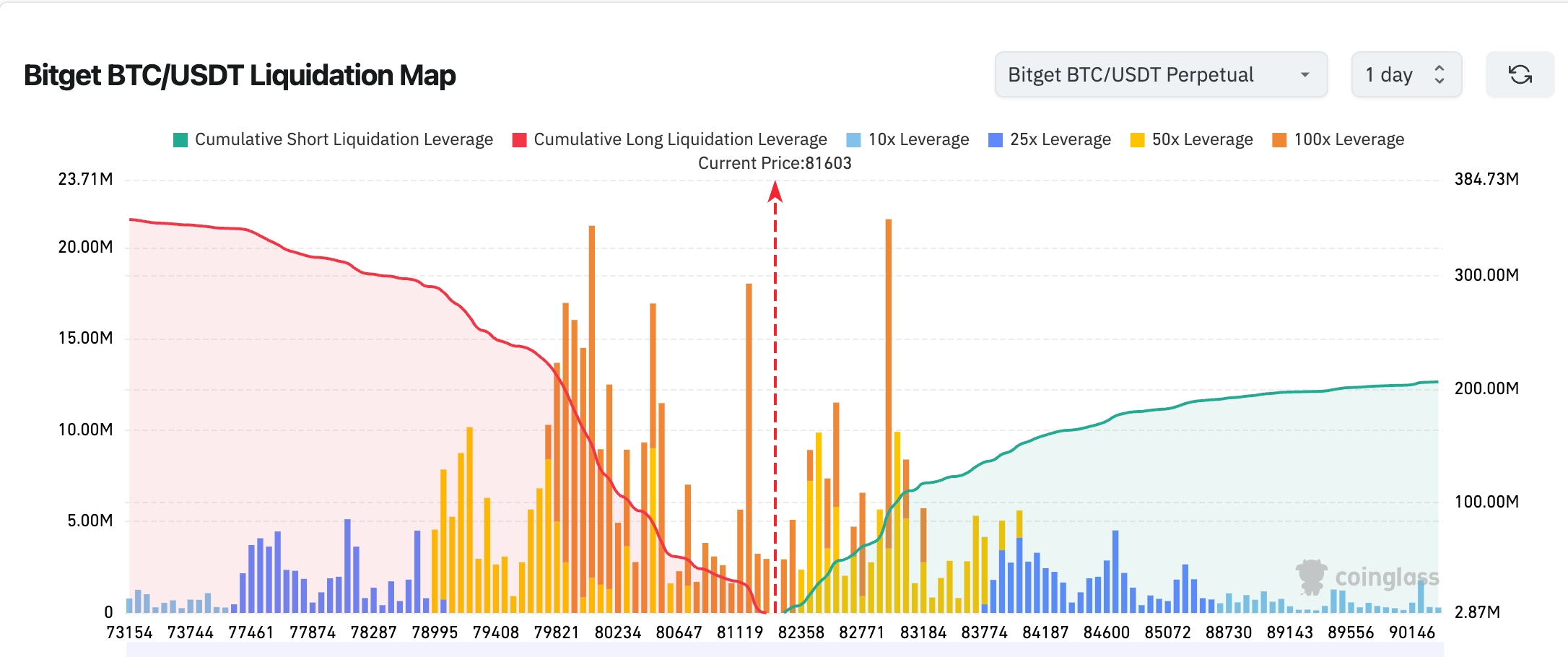

- Bitget BTC/USDT Liquidation Heatmap: BTC is trading near $81,603. A heavy concentration of high-leverage short liquidation zones sits between $82,000–$83,000; further upside could trigger cascading short covering and amplify gains. Below, dense long-leverage clusters exist around $79,800–$80,500; a breach here risks a short-term long squeeze and rapid pullback.

US Stock Indices Performance

- Dow Jones: +0.02% at 49,609.16 points, trading in a narrow range with defensive characteristics prominent.

- S&P 500: +0.84% at 7,398.93 points, setting a fresh all-time high, driven by heavyweight technology names.

- Nasdaq: +1.71% at 26,247.08 points, also hitting a record high, clearly powered by the AI infrastructure theme.

Tech Giants Performance

- Apple (AAPL): $293.32, +2.05% (record closing high) — Intel potential foundry orders boosting supply-chain confidence.

- Microsoft (MSFT): $415.12, -1.34% — major hedge-fund reduction draws attention.

- Alphabet (GOOGL): $400.80, +0.71% — AI search and cloud businesses continue to attract capital.

- Amazon (AMZN): $272.68, +0.56% — steady e-commerce and cloud performance.

- NVIDIA (NVDA): $215.20, +1.75% — AI chip demand remains robust, yet capital is beginning to rotate elsewhere.

- Meta (META): $609.63, -1.16% — advertising business facing competitive pressure.

- Tesla (TSLA): $428.35, +4.02% — improved outlook for EV and robotics businesses.

Core Driver Summary: AI infrastructure investment thesis is broadening from single-chip focus to full-stack coverage; capital is rotating into memory, foundry services, and diversified hardware.

Sector Rotation Highlights

Semiconductor Sector up more than 10% (several stocks posting outsized gains)

- Representative names: Micron +15.49%, SanDisk +16.6%, AMD +11.44%, Intel +13.96%, Qualcomm +8.17%.

- Key Drivers: AI data centers are evolving from chatbots to intelligent agents; memory-chip shortages and surging global AI capex (ByteDance +25%) are fueling the move. Market attention has clearly shifted toward “beyond NVIDIA” infrastructure plays.

3. In-Depth US Stock Analysis

1. Lumentum (LITE) – Dawn of the Optical Interconnect Era

Event Overview: Lumentum will officially join the Nasdaq-100 on May 18, 2026 (pre-market), replacing CoStar (CSGP). As the leading optical-module supplier, its products are widely used in high-speed AI data-center interconnects. Market Interpretation: Institutions view the inclusion as confirmation of optical communications’ rising strategic importance in AI compute networks; data-center interconnect demand is expected to keep expanding. Investment Takeaway: AI infrastructure investment is extending from compute to transmission layers; optical-module leaders may enjoy a sustained growth window—track order flow and technology roadmaps closely.

2. Intel (INTC) – Apple Foundry Order Secured

Event Overview: Apple has reached a preliminary chip-foundry agreement with Intel, potentially ending TSMC’s monopoly on advanced nodes. Market Interpretation: Analysts see this as the strongest validation yet for Intel’s foundry turnaround, while also easing Apple’s AI capacity concerns and reshaping the global advanced-process landscape. Investment Takeaway: US onshoring of supply chains is accelerating; Intel and other domestic players still have valuation-repair upside, though execution risks remain.

3. Palantir (PLTR) – OpenAI/Anthropic Direct Competition

Event Overview: OpenAI is building a data-connection platform and replicating Palantir’s “forward-deployed engineer” model; Anthropic is also entering the fray with former Palantir staff on its team. Market Interpretation: William Blair analysts note that AI giants are intensifying pressure on Palantir’s core strengths; market-share battles have begun. Investment Takeaway: Competition in data analytics and AI deployment services is heating up; Palantir must accelerate product iteration to defend its lead.

4. Microsoft (MSFT) – Major Hedge-Fund Trim

Event Overview: Prominent hedge fund TCI slashed its Microsoft stake from 10% to 1%, ending nearly a decade of ownership, while lifting Alphabet to 5%. Market Interpretation: The fund believes AI poses a structural threat to Office and Azure, and Microsoft shares have already fallen more than 12% YTD. Investment Takeaway: AI is reshaping software and cloud economics; legacy giants must speed up transformation—investors should monitor business-structure adjustments.

4. Cryptocurrency Project Updates

- This week AVAX, STRK, SEI and others face large one-time token unlocks; AVAX will unlock 1.67 million tokens on May 12, valued at approximately $17.25 million.

- Digital Asset, the blockchain technology provider to major banks and trading firms, is raising a new round at a roughly $2 billion valuation, with a16z crypto among the investors.

- Analyst Yashu Gola notes that ETH/BTC has fallen more than 35% over the past year and is repeating the bearish pattern seen from 2024–2025. Technically, the pair remains capped by the downtrend line since 2022; multiple breakout attempts have failed, one triggering nearly 70% further downside. After testing the trendline again in August 2025 and breaking below the 20-month EMA near 0.034, bears remain in control. If weakness persists, the next downside target is around 0.0176—roughly 40% lower from current levels, corresponding to the 2020 cycle low.

- CryptoQuant analyst Axel Adler Jr. remains cautious on Bitcoin, viewing the current rally as a corrective bounce after the plunge rather than the start of a confirmed new bull market. Chain metrics have yet to reach typical bear-market bottom levels; long-term holder (LTH) positioning has not formed the classic accumulation pattern, and the market has not yet seen full spot capitulation and panic clearing.

- On May 10, Michael Saylor highlighted BTC-DeFi integration as one of his top trends. Yield-bearing tokens built on STRC are growing rapidly, with some protocols expanding TVL at $1 million per hour. Existing DeFi protocols using STRC already offer 8–11% yield products, further amplified by 3–5× leveraged loops. Saylor expects the yield-token market to become a multi-billion-dollar new industry in the coming months.

5. Today’s Market Calendar

Economic Data Release Schedule

| 10:00 | US | April Existing Home Sales | ⭐⭐⭐ |

| 10:00 | US | NFIB Small Business Optimism | ⭐⭐ |

Key Event Preview

- Circle Earnings: Released today; focus on stablecoin business and profitability.

- Cerebras IPO: Scheduled for May 14, oversubscribed 20×; pricing range may be raised.

Additional macro highlights this week center on US April CPI:

- Tuesday 15:15 (UTC+8): FOMC permanent voter and New York Fed President Williams participates in a monetary-policy panel.

- Tuesday 20:15: US ADP Employment Change for week ending April 25.

- Tuesday 20:30: US April CPI.

- Wednesday 04:30: US API Crude Inventory for week ending May 8.

- Wednesday 20:30: US April PPI (YoY & MoM).

- Friday 05:30: Fed Governor Barr speaks.

- Friday 21:15: US April Industrial Production (MoM).

The Fed will also see a major leadership change: nominee Kevin Warsh is expected to be confirmed by the Senate on Monday and officially succeed Chair Powell on May 15. US stock-index futures opened modestly lower Monday. Although Q1 earnings season is winding down, corporate reports will remain a key stock driver over the next few days.

Institutional Views

Multiple investment-bank analysts agree that markets are at a pivotal inflection: AI investment logic is shifting from “single-chip” to “full-stack infrastructure.” Previously undervalued segments such as Intel, Micron and AMD are seeing strong capital inflows, while NVIDIA remains dominant but shows early signs of “power rotation.” On the geopolitical front, the stalled Iran peace proposal is pressuring oil prices, yet the resumption of China-US trade talks provides a buffer for risk assets. Crypto markets continue to benefit from ETF inflows (despite short-term swings) and accelerating traditional-finance tokenization; BTC and ETH remain range-bound in the near term but retain a constructive medium-term bias. Overall, institutions expect near-term volatility to revolve around data and events, while longer-term AI capex upgrades (ByteDance +25%) and domestic supply-chain trends should underpin technology and related assets. Investors are advised to monitor sector rotation and maintain appropriate risk hedges.

Disclaimer: The above content is compiled through AI-based search and has been reviewed by humans for verification purposes only. It does not constitute any investment advice. Data in this article may contain unavoidable discrepancies—please refer to real-time market data for accuracy.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

SAGA fluctuates 44.9% in 24 hours: trading volume surges over 7 times and open interest rises, driving a rebound

SKYAI (SKYAI) fluctuates 59.8% in 24 hours: Whale accumulation and trading volume surge trigger sharp volatility

Emerging markets: Broadening gains persist in 2026 – HSBC