The era of "dual dominance" in HBM is approaching? UBS: Samsung's market share may catch up with SK Hynix next year

The AI computing power arms race continues to intensify, and the landscape of the HBM (High Bandwidth Memory) market is quietly undergoing changes.

According to the latest UBS research report, by 2027, Samsung is expected to be neck and neck with SK Hynix in HBM bit shipments, each occupying about 40% of the market share, while Micron will account for around 20%. This represents a historic reshaping of the HBM market and holds significant implications for related investors.

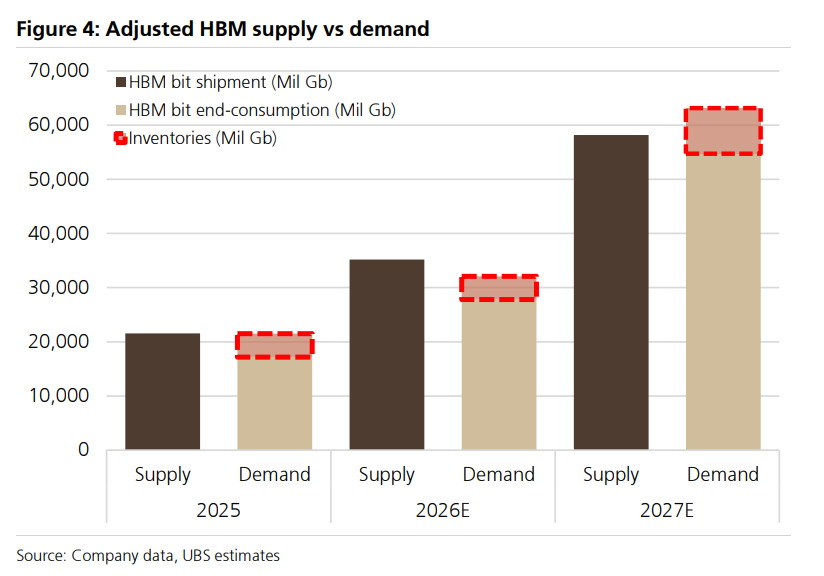

On the demand side, UBS has raised its forecast for HBM end market bit demand in 2026 from 31.5 billion Gb to 32.9 billion Gb (an 88% year-on-year increase), and for 2027 from 53.9 billion Gb to 58.0 billion Gb (a 76% year-on-year increase). The main revision stems from an increased assumed Google TPU purchase volume.

Meanwhile, the HBM configuration of Nvidia Rubin Ultra has been revised downward from the previously assumed 1TB (HBM4E 16-Hi) to 768GB (HBM4E 12-Hi) (UTC+8). The report notes that this "remains an evolving situation and there is no final decision yet," suggesting that Nvidia is proactively working to avoid supply bottlenecks and is preparing for the yield challenges of the 16-Hi stacked thermal compression bonding process.

On the pricing front, the increase in server memory prices also exceeded expectations. UBS has raised its Q2 DDR contract price growth forecast significantly from +37% to about +60% (quarter-on-quarter). Average server DDR prices are expected to reach $1.95 per Gb (UTC+8), with some DDR5 quotes approaching $2.10 per Gb (UTC+8), a sharp jump from the $1.15 in Q1. The Q3 price hike forecast remains at +10%, and server DDR prices are expected to be close to $2.80/Gb (UTC+8) by Q4 2027. For NAND flash, the Q2 binding contract price increase forecast has also been raised from +40% to +60% (UTC+8), also driven by server SSD demand.

Samsung in Strong Pursuit, Expected to Tie with SK Hynix in 2027

Samsung's pushback in the HBM field is the main narrative worth watching in this report.

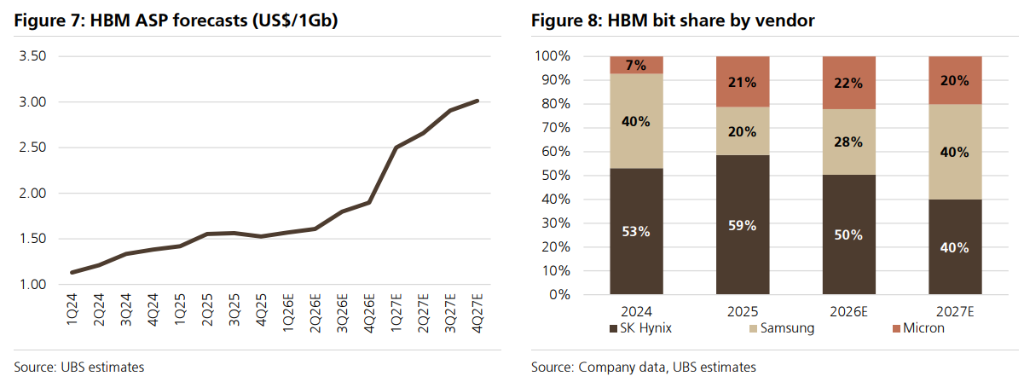

UBS maintains its forecast for Samsung's HBM shipments in 2026 at 9.7 billion Gb (a 124% year-on-year increase), but has significantly raised the 2027 projection from 20.3 billion Gb to 23.0 billion Gb (a 137% year-on-year increase), which is supported by Samsung’s recent advance capital expenditures. If the forecast materializes, Samsung and SK Hynix will each hold 40% of the HBM bit market share in 2027, achieving a tie.

In contrast, UBS has slightly lowered its HBM shipment forecast for SK Hynix—2026 is revised down from 18.4 billion Gb to 17.7 billion Gb (a 40% year-on-year increase), and 2027 from 24.7 billion Gb to 23.1 billion Gb (a 30% year-on-year increase).

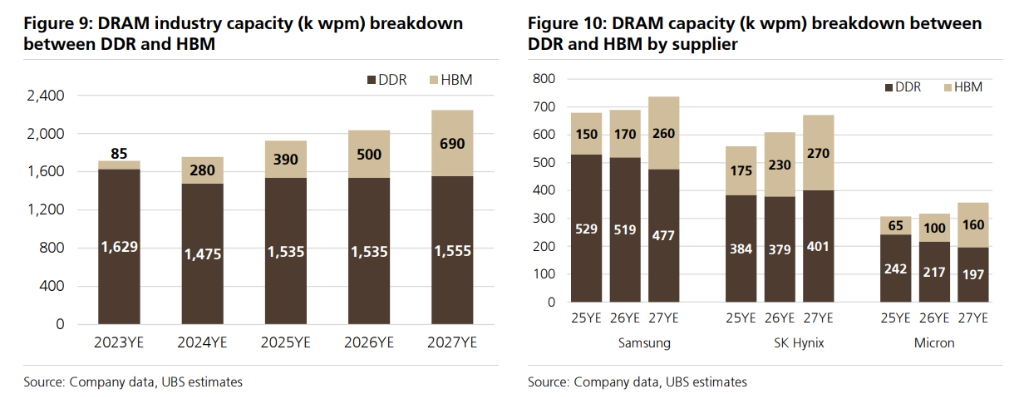

The reason is not a weakening of HBM competitiveness, but rather continuous and strong customer requirements for SK Hynix to shift more capacity toward DDR5 and LPDDR5X. The report explicitly emphasizes that HBM4 is not a supply bottleneck for the Rubin product line expected to ramp up in the second half of the year.

Differentiated Demand Structure: Nvidia's Dominance Decreases, Google's Share Rises Rapidly

Looking at customer structure, Nvidia will still account for about 60% of HBM demand in 2026 (UTC+8), but this share will drop to 48% in 2027 (UTC+8); Google's share will rise from 19% in 2026 (UTC+8) to 27% in 2027 (UTC+8), corroborated by the simultaneous increases in UBS’ forecasts for Broadcom and MediaTek.

By product generation, HBM3E 12-Hi will account for 47% (UTC+8) in 2026, while by 2027, HBM4 will become the core product (44%) (UTC+8), with HBM4E making up 21% (UTC+8). For pricing, the assumed average price per bit of HBM4/HBM3E in 2027 has been raised from flat to a year-on-year increase of 30% (UTC+8), while the premium of HBM4E over HBM4 remains at +50%.

Overall, the UBS monthly report delivers a clear signal: the boom in AI infrastructure construction is still accelerating, the memory supply-demand balance remains tight, and the pricing focus is moving upward across the board; Samsung’s catch-up is rapidly reshaping the HBM competitive landscape, and a dual oligopoly may arrive sooner than the market expects.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Forex Today: US Dollar holds ground, focus shifts to Trump-Xi summit

A8 (Ancient8) price surged 50.2% in 24 hours: trading volume spikes drive short-term volatility