"Global Anchor for Asset Pricing" Poised for a Strong Comeback? 30-Year US Treasury Auction Yield Returns to 5% After Nearly 20 Years

According to Zhitong Finance, as global energy prices surge, significantly pushing up domestic US inflation and boosting financial markets’ pricing expectations for future inflation rates and even the restart of Federal Reserve rate hikes, bond market investors have, for the first time since 2007, secured yields as high as 5% in the 30-year US Treasury auction. This highlights the resurgence of inflation and stagflation concerns in a macroeconomic context marked by ongoing geopolitical conflict in the Middle East. Coupled with a wave of "populist" policies, the US budget deficit and debt interest scale continue to expand, and the largest buyer, Japan, has dumped US Treasuries at the largest scale in nearly four years. Investors are demanding higher yields to compensate for these numerous risk factors before they are willing to hold long-term US Treasuries.

The final winning yield for the 30-year US Treasury auction was 5.046%, which means that the long-term US Treasury yield curve—deemed the "anchor of global asset pricing" and currently near 4.5%—suggests that the 10-year Treasury yield in the secondary market could potentially move toward 5%, the highest level for the 10-year Treasury since October 2023. This 30-year Treasury auction continues the overall pressured state of US government bond issuance this week. Both the 3-year and 10-year US Treasury auctions earlier in the week saw significantly lower demand than both Treasury and market consensus expectations, collectively indicating that buyers are now demanding higher yields to compensate for higher inflation and larger supply risks.

On the trading and pricing side of financial markets, the 10-year US Treasury yield serves as the undisputed "anchor for global asset pricing." If, over the coming period, this yield indicator continues to rise due to stronger inflation expectations and "term premium" factors driven by greater fiscal stimulus, and approaches that key psychologically significant 5% level, it will undoubtedly push up the risk-free rate parameter in DCF quant valuation models for risky assets. This could lead to a reduction—or even collapse—of overall valuations for unprofitable popular tech and growth stocks, momentum stocks linked closely to the AI computing power theme, high-yield corporate bonds, and cryptocurrency assets. Furthermore, if the 10-year Treasury yield keeps rising along with inflation instead of growth improvement, corporate profit margins will be further squeezed by energy, wage, and financing costs.

The so-called term premium refers to the extra return that investors demand for holding long-term bonds due to associated risks. A 2025 IMF policy study clearly found that, after a marked deterioration in fiscal conditions, the link between deficits and interest-bearing debt with higher long-term interest rates and higher term premia has significantly strengthened.

According to some economists, the term premium indicators for government bonds in developed countries will be much higher in 2026–2027, especially as Trump 2.0-era US Treasuries and budget deficits could exceed official forecasts by a large margin, primarily due to a new administration under Trump focusing on a “domestic tax cut + external tariff increase” economic growth and populist protectionist framework, combined with swelling budget deficit, Treasury bond interest payments, and military-industrial defense spending catalyzed by Middle East geopolitical conflict. The US Treasury's bond issuance scale may be forced to expand even more than under the spendthrift Biden administration in this "Trump 2.0 era," inevitably making the "term premium" much higher than in the past.

US Treasury auction sounds the global pricing alarm! For the first time since 2007, buyers of long-term US Treasuries get 5% yield

Reportedly, on Wednesday Eastern US time, the $25 billion new 30-year Treasury auction had a winning yield of 5.046%, a rate determined by the yield most bidders were generally willing to accept. This result was slightly higher than pre-auction real-time market pricing, indicating exceptionally weak demand as US government bond yields rose to their highest levels in nearly a year. Both 3-year and 10-year Treasury auctions earlier this week also saw much less demand than expected. The key "5.046%" here refers to the winning/highest yield in the new 30-year Treasury auction, not the coupon rate itself.

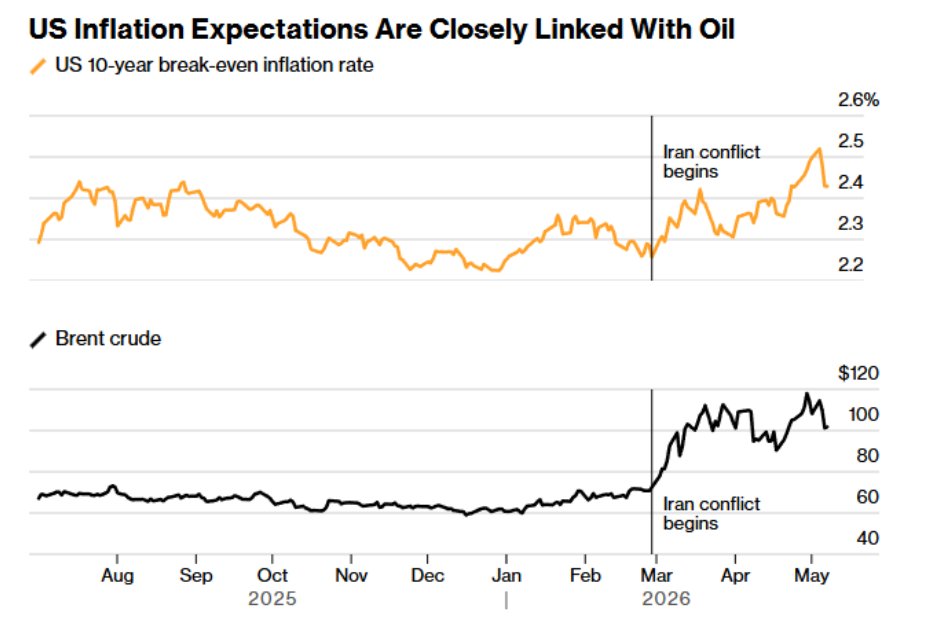

All this shows that auction bidders are demanding higher fixed yields to compensate for risks such as high benchmark rates, further accelerating inflation, and expanding fiscal spending. Since the US and Israel jointly struck Iran at the end of February, leading to major disruptions in Middle East oil and natural gas supply, energy price increases have fueled inflation. The oil price shock has escalated broad indicators of inflation, including the Consumer Price Index and Producer Price Index, and raised market-based long-term inflation expectations and the odds of further Fed rate hikes.

Wednesday's much-stronger-than-expected April PPI data further reinforced the sharp reversal in Fed policy expectations triggered Tuesday by the CPI report. According to the latest CME FedWatch pricing, the market has basically priced out any possibility of a rate cut between now and the end of 2027. Instead, the probability of a 25 basis point rate hike by year-end has risen to around 50% (from about 37% on Tuesday), and money market pricing expects a cumulative 24 basis points of Fed rate increases by the June 2027 meeting.

Deutsche Bank senior rates strategist Steven Zeng said, “I expect at a long-term (10 years and above) Treasury benchmark yield of 5%, investor demand will begin to emerge. Usually, at this level, 30-year US Treasuries become more attractive to pension funds and other liability-driven institutional investors.” However, Zeng noted, this depends on whether inflation will force the Fed to hike rates, and futures markets have started to price in this possibility.

He added: “Our base case is that the Fed is done with rate cuts but will not move to hikes, as long-term inflation expectations remain well-anchored. But if high energy prices unanchor expectations, the market will have to rethink the Fed’s monetary policy path, and that would be a scenario for a sharp move higher in yields.”

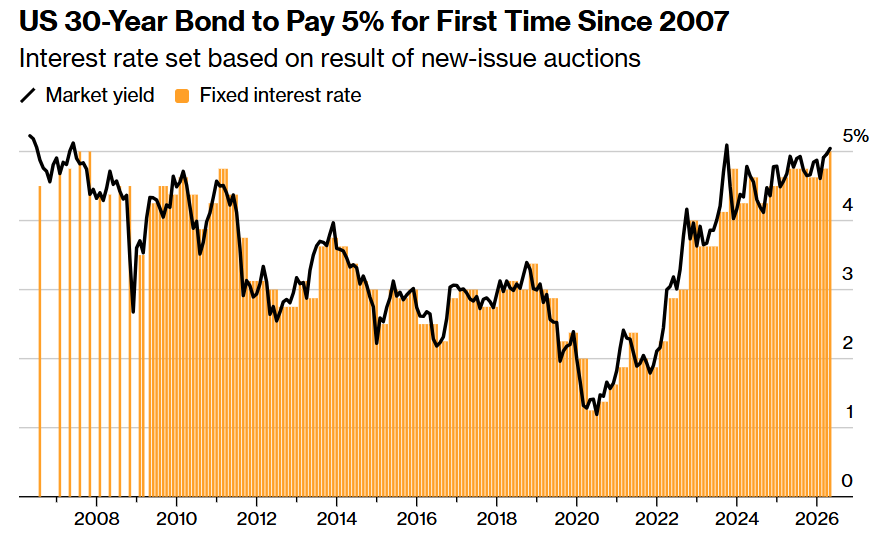

As shown above, the US 30-year Treasury is paying 5% for the first time since 2007—yields decided by the results of new issue auctions.

The last 30-year Treasury with a 5% yield was issued in 2007, just before the global financial crisis and the US recession. Since then, no 30-year Treasury auctioned has yielded higher than 4.75%. The lowest 30-year Treasury yield over the past 20 years was 1.25%, set during a May 2020 auction under the post-COVID-19 global pandemic and the Fed’s quantitative easing campaign. To attract buyers, such long-duration bonds are now even trading in the market at less than 50 cents on the dollar.

The fixed rate on Treasury notes and bonds is set by the auction result, and an auction outcome between 5% and 5.124% means the coupon rate is 5%.

This is not the only US Treasury security auction in the last 20 years to have a yield reaching 5%. The 20-year Treasury, reissued by the US government in 2020, has mostly yielded more than the 30-year bond since its comeback, reflecting weaker investor demand. For example, a 20-year Treasury to be issued in May 2025 has a yield of about 5%.

In recent years, US government long-term security asset auctions have on multiple occasions traded above 5% in the secondary market, first breaking the threshold in October 2023, when the Fed had hiked rates by more than five percentage points to curb an earlier inflation surge. The expansion of Treasury auction volumes and the sharp increase in interest-bearing government debt also contributed to this move.

With 30-year US Treasury yields hitting 5% for the first time since 2007, the "anchor of global asset pricing" stands ready to shake things up

Since 2007, global bond investors have for the first time secured 30-year US Treasury yields of as high as 5%, and the latest market news shows that the biggest single buyer, Japanese institutions, are withdrawing from the US Treasury market at the fastest pace in nearly four years—according to the latest Ministry of Finance balance of payments data released Wednesday, Japanese investors had net sold 4.67 trillion yen ($29.6 billion) in US Treasuries, agency, and muni bonds in the three-month period ending March 31, the highest quarterly reduction since Q2 2022—implying that the risk of further yield surges in the relatively shorter-term 10-year Treasury has yet to be fully released.

The US Treasury market is shifting from a “rate-cut trade” to a new framework of “inflation repricing + term premium fully priced-in + populist fiscal policy + weakened foreign buying.” The winning yield for the 30-year Treasury was 5.046%, the first time since 2007 that a new 30-year bond offered a 5% return; meanwhile, 3-year and 10-year auctions were also weak, all indicating that buyers are now requiring higher yields to compensate for inflation and fiscal supply risk.

More crucially, it is not only nominal rate expectations but also higher inflation expectations that are driving up yields. The energy price shock is filtering through gasoline, diesel, transportation, food, and the PPI chain into broader prices. After the April PPI beat expectations, the 10-year Treasury yield briefly rose to around 4.5%, and the 30-year yield moved above 5%. If the market starts believing the energy shock is not a “one-off event” but will unanchor inflation expectations, the Fed’s policy path will be repriced from “rate cuts are done” toward “a tail risk of resumed Fed hikes.”

Steven Barrow, head of G10 strategy at Standard Bank in London—known as a "senior bond market hunter"—predicts the 10-year Treasury yield may reach 5% this year, with the core logic similar to the above: persistent inflation, fiscal expansion, and a repricing of the Fed policy path. This level is not the market’s consensus median, but rather a contrarian/hawkish tail risk; yet given the present combination of oil shocks, fiscal deficit, bigger bond supply, and weaker overseas demand, that prediction is gaining credibility. If the 10-year does make a true break above 5%, it will not just be a bond market event, but a “denominator shock” to the entire global risk asset valuation system.

Steven Barrow’s bearish US Treasury predictions in 2021 proved prescient, as the recovering economy drove yields higher. In recent years, he also successfully forecast USD and GBP trends, though he misjudged the persistent weakness of JPY. “This view isn’t just driven by war, though it is reinforced by it,” Barrow said, “The Fed may keep policy too loose, structural inflation pressures are rising, and I don’t think government will do anything about the budget.”

The 10-year Treasury yield is known as the "anchor of global asset pricing." If this yield continues to rise due to fiscal stimulus-driven term premium, it will almost certainly cause another collapse in high-yield corporate bonds, the tech stocks most closely linked to AI driving the global equity bull market, and even cryptocurrencies and other top-performing risk assets globally. If longer-term (10 years+) Treasury yields keep climbing, it means “significantly higher capital costs + weakening liquidity expectations + macro denominator expansion” all happen at once for stocks, cryptocurrencies, and high-yield bonds.

If the 10-year yield stays high due to increased term premium or if bond market volatility rises, the discounted future cash flows of AI-linked tech stocks will become more stringent, placing particular pressure on “AI concept assets” whose valuations depend on realization of future profits or for which free cash flow is not yet well established.

Theoretically, the 10-year Treasury yield is the risk-free rate (r) in major DCF valuation models for the stock market. If other parameters (especially future cash flow forecasts, i.e., the numerator) remain unchanged—like during earnings season when the numerator is in a catalyst vacuum—a higher or persistently elevated denominator level threatens to collapse the valuation of those AI-linked tech stocks, high-yield corporate bonds, and cryptocurrency risk assets trading at historical highs.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

DODO fluctuates 41.9% in 24 hours: technical channel breakout and low liquidity drive

Official XRP Ledger-JPMorgan Integration Now Active

US Dollar Index: Downside risks despite delayed easing – TD Securities

US Morning News Call | President Trump Meets Chinese Leader Xi Jinping in Beijing Summit