How much impact will the strike have on Samsung? JPMorgan: Any pullback is a buying opportunity

Samsung Electronics is facing the threat of a large-scale strike, but JPMorgan believes the strong rise in memory prices is sufficient to offset most of the shock, so the logic of buying on dips still holds.

According to Chasing Wind Trading Desk, on May 13, a research report from Jay Kwon’s team at JPMorgan pointed out that if a large-scale strike at Samsung occurs as scheduled, it will impact Samsung’s 2026 operating profit by 2.1 to 3.5 trillion KRW and drag down semiconductor division revenue by about 1% to 2%.

However, JPMorgan maintains its “Overweight” rating on Samsung Electronics and explicitly states that “For any share price corrections triggered by strike issues, we continue to recommend buying on dips.”

The report highlights that second quarter DRAM contract prices rose quarter-on-quarter by 58% to 63%, while NAND surged 70% to 75%—well above JPMorgan’s previous expectations of 40% to 50%. The stronger memory price cycle is expected to largely hedge labor cost pressure.

Mediation Collapses, Strike Imminent

This week, government-led labor negotiations in South Korea broke down, with Samsung Electronics management and the National Samsung Electronics Union (NSEU) failing to bridge their differences.

NSEU subsequently announced an 18-day all-out strike from May 21 to June 7, with about 50,000 union members expected to participate—exceeding the 37,000 to 40,000 participants in the rehearsal held at the Pyeongtaek chip campus on April 23.

The core dispute between labor and management centers on two points: removing the cap on Operating Profit Incentives (OPI) and legalizing the profit sharing incentive mechanism.

JPMorgan analyst Jay Kwon pointed out that after the government mediation period from May 11 to 12, the positions of both sides did not significantly narrow.

Samsung has already applied to the courts for an injunction against possible illegal industrial action by the union and is awaiting a decision by May 21, but the outcome remains uncertain.

JPMorgan lists the court’s ruling before May 20 and the potential for an emergency mediation order as the next key event nodes. Several South Korean policymakers have voiced concerns about how the strike may threaten the stability of the national AI supply chain.

The Minister of Employment and Labor in South Korea may issue an “emergency mediation order” under statutory conditions, with the power to forcibly suspend strike action for 30 days.

JPMorgan notes that there have only been four such precedents in the past 57 years—the most recent being the Korea Airline Pilots’ Association strike in December 2005.

Financial Forecasts, Full-Year Operating Profit Could Take a Hit of Up to 3.5 Trillion KRW

According to JPMorgan’s latest analysis, if Samsung accepts the union’s demands to allocate 10% to 15% of operating profits to OPI incentives and increase base salaries by 5%,

labor costs for 2026 will rise by 1.69 to 3.04 trillion KRW compared to earlier estimates. Adding an estimated sales opportunity loss of about 4.5 trillion KRW, the overall impact on operating profit is estimated at 2.1 to 3.5 trillion KRW.

JPMorgan believes that under a 10% to 15% OPI share scenario, there is a 3% to 7% downside risk for operating profit.

Based on revenue impact calculations, an 18-day strike is expected to result in an annualized reduction in DRAM shipments by about 1.0%, NAND by about 0.5%, foundry and system LSI business by about 2.1%, with the semiconductor division’s revenue affected by a total of about 1% to 2%.

If the strike impact worsens, with daily memory and foundry wafer capacity affected by 40% and 75% respectively nationwide, lost revenue opportunities could reach as high as approximately 9 trillion KRW.

It’s worth noting that compared to the estimate on May 6, the impact from increased labor costs has narrowed slightly, as JPMorgan performed a more refined recalculation of employee compensation structures and OPI pools for each segment.

However, production impact has been revised slightly up due to the expected higher participation than the April 23 rehearsal.

Memory Price Surge May Become Key Hedging Factor

JPMorgan believes that the current trend in memory prices may be the largest hedging variable.

The research report, citing media reports, states that Q2 contract DRAM prices rose 58% to 63% quarter-on-quarter, and NAND prices rose 70% to 75%. The main drivers are the rising demand for CPU memory and tightening supply of LPDDR5X.

JPMorgan notes that a higher Q2 profit baseline helps offset the impact of rising labor costs. At present, market investors appear to be pricing in an “optimistic scenario,” where the strike could instead catalyze positive momentum in contract price negotiations for Q2 and Q3.

JPMorgan’s 2026 earnings forecast was already higher than the Bloomberg consensus, with JPMorgan projecting DS (semiconductor) segment revenue of 47.09 trillion KRW versus consensus at 44.32 trillion KRW. The DRAM average selling price increase is forecasted at 260%, well above the consensus estimate of 219%.

Short-term Pressure, Unchanged Long-term Logic

JPMorgan admits that strike-related uncertainty could suppress the stock price in the short term, and does not rule out that Samsung might underperform memory peers.

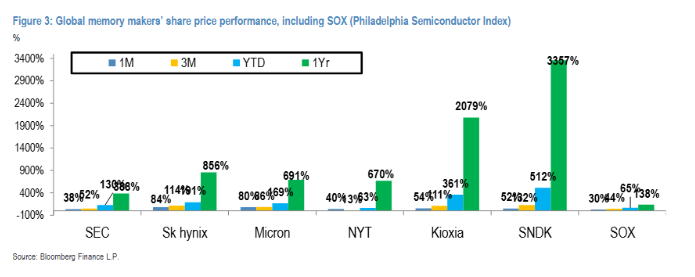

Data shows that since April, Samsung Electronics’ share price has risen by around 60%, while SK Hynix surged by about 122% in the same period, and Korea’s composite stock price index rose about 48%.

But JPMorgan’s medium- and long-term thesis remains unchanged: the memory upswing cycle is “higher and more durable,” with sustained improvements in HBM (High Bandwidth Memory) execution.

The current target price is based on a 2026–2027 forecast price-to-book ratio of 2.2x, a 10% premium to the peak cycle historical P/B, to reflect the multiyear memory upcycle and improved momentum in foundry orders.

Analysts also caution about downside risks, including: a prolonged memory price downcycle, weaker-than-expected HBM demand from ASIC customers, and delays in future HBM product certifications.

~~~~~~~~~~~~~~~~~~~~~~~~

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US Dollar Index steadies following news of positive Trump-Xi summit

US Dollar Index: Supported but capped on topside – OCBC

New Zealand Dollar consolidates with a bearish tilt as domestic economic risks increase