CNY: 6.8 is not the end

After more than half a month of tug-of-war, USDCNY has finally broken below the 6.8 mark. Looking ahead, I believe 6.8 is not an end, but rather a new beginning.

Firstly, compared to “RMB appreciation”, the trend since April is more about “USD weakness”. From the perspective of a basket of non-USD currencies, the RMB has actually depreciated since April. The RMB has risen by 1.6% against the USD, which still does not exceed the extent to which the USD Index has weakened (2%). This partly explains the policy's “resilience”: The April Politburo meeting's rhetoric on exchange rate stability did not show significant strengthening, and the Q1 monetary policy report released on the evening of May 11 added the statement of “maintaining exchange rate flexibility”.

Secondly, there are some common patterns in the behavior of USDCNY around China-US leader summits based on historical experience. After major face-to-face meetings such as the Busan Summit and the San Francisco Summit, market expectations for marginal improvements in China-US bilateral relations often drive USDCNY downward; after Trump’s last visit to China (December 2017), USDCNY even dropped from 6.6 to the low point of 6.3.

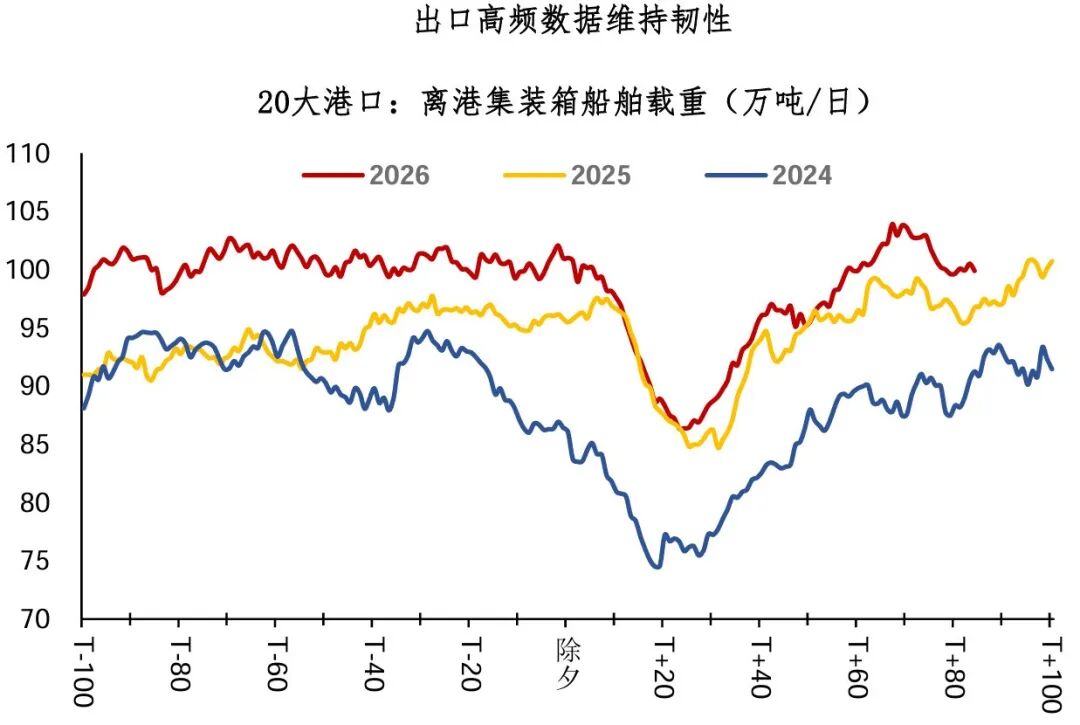

Additionally, high-frequency export data remains resilient. After the disturbance of the Spring Festival, high-frequency data such as outbound vessel tonnage has stayed relatively strong in Q2; April exports announced by the General Administration of Customs surged by 14%. Considering that last year’s base was already high, Q2 exports are holding firm. Combining with market conditions, I believe foreign exchange settlements may still outperform the average in previous years. Of course, since summer is the season for dividend purchases of foreign exchange, the power of such settlements may marginally weaken.

Lastly, April’s price data actually came in above expectations, suggesting monetary policy may remain on hold for an extended period. Compared to the PPI figure of 2.8%, the greater surprise lies in the speed and breadth of price transmission to mid- and downstream industries: more than 70% of PPI sub-items have picked up, and core goods CPI (communication devices 4.2%, home appliances 2.6%, etc.) also improved. With economic growth at the upper end of the targeted range and nominal growth recovering, the urgency for broad easing is evidently lower.

Some people in the bond market compare the recent trend with the “asset shortage” of 2016, but considering both domestic and international environments, I think today’s market situation is somewhat similar to the second half of 2021. If both Chinese and US policy rates remain unchanged, RMB may continue to appreciate steadily due to the current account impact.

To summarize today’s sharing:

1. After more than half a month of tug-of-war, USDCNY broke below the 6.8 mark. Looking forward, 6.8 is not an end but a new beginning. Since April, RMB hasn’t significantly appreciated against a basket of currencies, and policy may remain resilient; before and after China-US summits, market expectations for improvements in China-US relations often drive USDCNY downward.

2. From the fundamentals perspective, China’s exports have remained strong recently; imported inflation is gradually being passed downstream, and with nominal growth recovering, the urgency for broad easing is clearly low. If both China’s and US’s policy rates remain unchanged, RMB may continue to steadily appreciate under the influence of the current account.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Euro flatlines above 1.1700 with ECB Lagarde, Trump-Xi summit on focus

Forex Today: Markets stabilize ahead of mid-tier US data, await news from Trump-Xi summit