Mid-Year Currency Market Review: Shadows Under the Scorching Sun

Morning FX

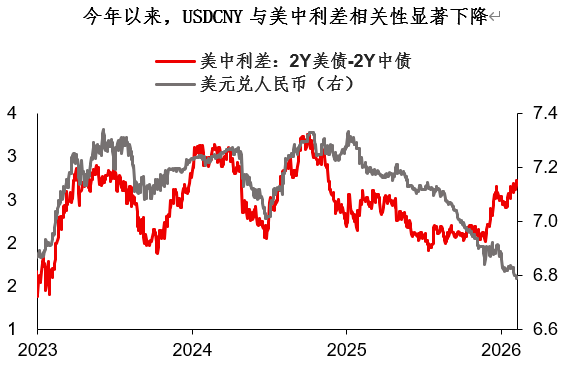

This year, there is an interesting phenomenon in the forex market—the correlation between many currency pairs, including the RMB, and interest rate differentials has significantly decreased. It feels as if the entire market is revolving around the stock market and risk sentiment.But beneath the scorching sun, there are also some little-known shadows.

Based on the prevailing mainstream market views and pricing data, the second half of the year may be characterized by sticky oil prices and sticky interest rates. Given that financial fragility already exists, a necessary inference is that some exogenous variables (such as political elections) could trigger tightening in financial markets. In fact, there is a political event in Europe in the second half of the year that is significantly more important than the UK local elections—the French Senate election (late September). This is another potential flashpoint for financial market vulnerability…

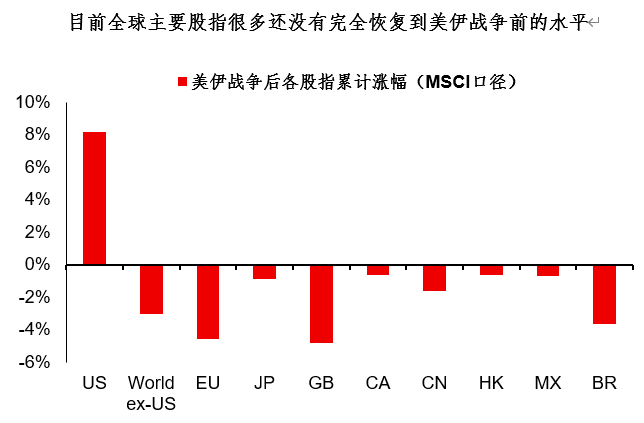

Some argue that high oil prices are not a big deal, as continued stock market increases can “cure all ills.” Such a view is perhaps overly optimistic—from MSCI data, most global stock indices have yet to fully recover to pre–US-Iran war levels. Moreover, only a handful of indices become cheaper as valuations rise; for most, higher valuations simply mean stocks are getting more expensive, and at a certain point, “rising” itself becomes the risk.

To summarize today’s sharing:

1. This year, there is an interesting phenomenon in the forex market—the correlation between many currency pairs, including the RMB, and interest rate differentials has significantly decreased. It seems the entire market floats around risk sentiment, yet beneath the scorching sun, there remain little-known shadows;

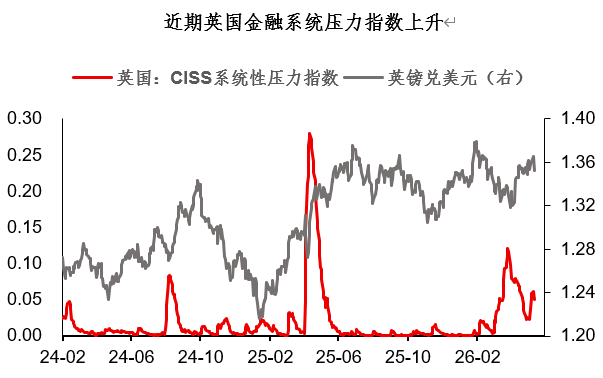

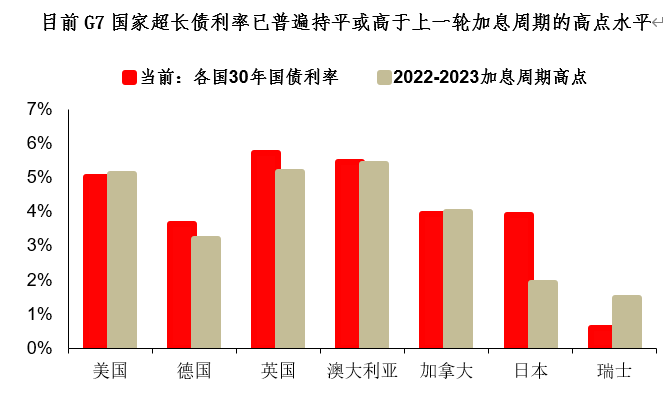

2. The UK Financial Stress Index (UK CISS) has surged recently. Ultra-long bond yields in G7 countries have now generally matched or exceeded the highs of the 2022–2023 rate hike cycle. Clearly, fragility objectively exists. If the second half of the year’s global baseline assumption is sticky oil prices plus sticky rates, such fragility is expected to persist;

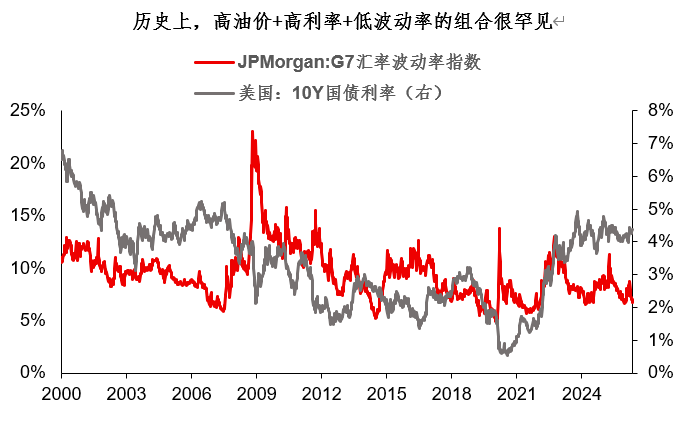

3. Currently, forex G7 volatility is at an extremely low level, historically just the 10th percentile. Looking at history, the combination of high oil prices, high rates, and low volatility is very rare. Is this tranquility from persistently rising stock prices, or compression before a spring rebounds? I tend to believe, from the perspective of risk balance, that the USD exchange rate may not be weak in the second half of the year, and could even strengthen somewhat. Meanwhile, after a round of shakeout in gold, its safe-haven properties may gradually return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BILL (BillionsNetwork) fluctuates 40.6% in 24 hours: trading volume soars to $666M with a 36% increase