Starmer "in danger", GBP and UK government bonds crash again, does the "British Empire" still have hope?

Another shock in British politics, with the markets reacting first and foremost.

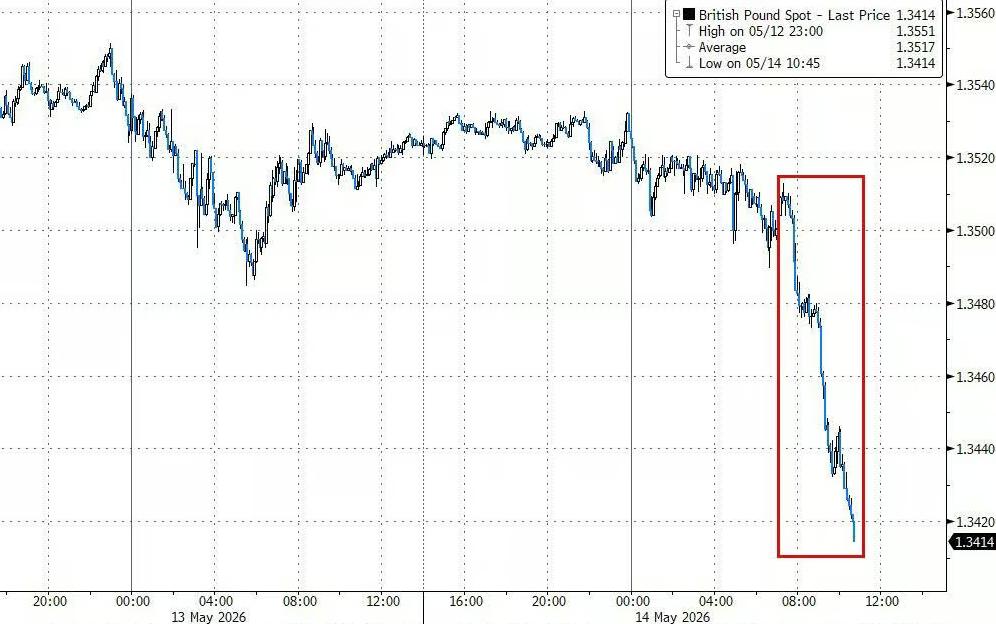

From May 14 to 15, as Prime Minister Starmer's leadership crisis suddenly escalated, both the pound and UK government bonds came under pressure. Health Secretary Wes Streeting publicly resigned, and Manchester Mayor Andy Burnham announced he would seek to return to Parliament, paving the way for a leadership challenge. The pound dropped nearly 1% in a single day to $1.3403, its lowest since April 13 and the largest weekly decline since January 2025. Meanwhile, the 30-year UK government bond yield climbed above 5.8% on May 12, marking its highest level in nearly thirty years.

The market's logic is straightforward: the likelihood of Starmer stepping down is rising, and his potential successors generally favor looser fiscal policies, meaning the British government may borrow more and issue more debt. Bond investors are highly alert to this.

According to Bloomberg Economics, in the few days between May 8 (when local election results were announced) and May 12, the increase in bond yields was already enough to add an extra £2 billion (around $2.7 billion) in debt interest payments by the end of this decade.

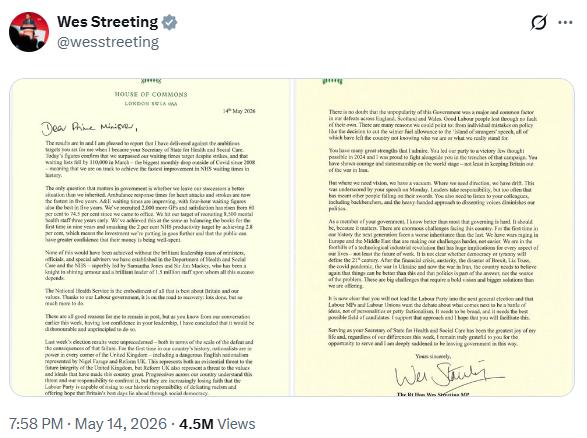

Resignation Letter Causes Uproar

Wes Streeting’s resignation letter was direct and ruthless in its wording.

"As you know from our conversation earlier this week, as I have lost confidence in your leadership, I believe it would be dishonest and without principle to remain in my post," he wrote in the letter.

He further pointed out that last week’s local election result was "unprecedented," the government’s "unpopularity" being a "key common factor" across the UK, and directly criticized Starmer: "We need vision, but there is only a vacuum; we need direction, but there is only drift."

Streeting is widely believed to be interested in running for Labour leader, though he did not formally declare his candidacy in his resignation letter.

Meanwhile, Manchester Mayor Andy Burnham was more concrete in his actions. Labour MP Josh Simons announced his resignation from his parliamentary seat in the Manchester area to make room for Burnham to run. In his statement, Simons wrote: "I am stepping aside so Andy Burnham can return to his hometown, re-enter Parliament and, if elected, drive the urgent change this country needs."

Burnham subsequently stated he would seek approval from Labour’s National Executive Committee to contest the seat.

Why is the Bond Market So Sensitive?

To understand why the market is so sensitive to British politics, one must first understand the central role of UK government bonds (gilts) in public finance.

In simple terms: if the government spends more than it collects in taxes, it must borrow from bond investors. The cost of borrowing is the interest paid, i.e., the yield. The higher the yield, the greater the government’s repayment pressure, and the less money is left for public services.

In the latest fiscal year, the UK government spent nearly £100 billion just on debt interest, according to data from the Office for Budget Responsibility—an amount comparable to the government’s annual education budget.

Currently, the 30-year UK government bond yield is around 5.7% to 5.8%, far higher than bonds of equivalent maturity in Europe and other developed countries. Multiple factors are behind this: inflation in the UK is more stubborn than in other countries, so the Bank of England maintains relatively high interest rates; Middle East wars have driven up energy prices, and the UK, being highly dependent on energy imports, is particularly affected.

In addition, the UK bond market itself is structurally fragile. Compared with the US Treasury market, the UK bond market is smaller, so even small trades can trigger significant price swings. Pension funds, previously stable holders of government bonds, have in recent years shifted toward equities and other risk assets, while the Bank of England has moved from buying large amounts of bonds to selling down its portfolio. Hedge funds and foreign investors now make up a higher share of the market, and when these types of investors feel uneasy, they are usually first to sell off.

"There are now more yield-sensitive buyers of UK government bonds," noted Rufaro Chiriseri, Head of Fixed Income at RBC Wealth Management. "The market will continue to generate more noise."

Fiscal Rules Are the Core Controversy

During their tenure, Starmer and Chancellor Rachel Reeves’ core policy commitment has been a set of self-imposed fiscal rules: routine spending must be matched by tax revenue, and the government may only borrow for investment purposes. The aim of these rules is to signal to bond investors that the government won’t borrow excessively.

But these rules have caused ongoing friction within the Labour Party.

Andy Burnham has publicly criticized the government’s economic direction, stating the UK is "held hostage by the bond market." He further proposed that additional borrowing could fund defense spending, circumventing current fiscal rules.

Another potential contender, Angela Rayner, has tried to assure investors that Labour will maintain fiscal discipline, but she previously led cabinet opposition to Reeves’ plan to cut welfare spending.

Even Streeting, seen as relatively moderate, has publicly stated his discomfort with the UK’s tax burden level.

Bloomberg Economics analysts Dan Hanson and Antonio Barroso wrote: "A change in leadership could amplify this trend, compressing fiscal space and becoming another headwind for a UK economy already struggling amid energy shocks."

Nomura strategist Dominic Bunning said he would be closely watching for any statements from Burnham regarding his fiscal stance in the coming days: "If the sell-off continues, even at a slow pace, people will question him about why his announcement triggered this sell-off and whether he wants to reconsider his comment about being 'held hostage by the bond market'," Bunning said.

The Shadow of the “Truss Moment” Remains

The bond market’s sensitivity to political risk is inextricably linked to the crisis of 2022.

That year, then Prime Minister Truss introduced a "mini-budget" featuring £45 billion in unfunded tax cuts, directly triggering a collapse in the bond market, causing the pound to fall to a record low and forcing the Bank of England into emergency bond purchases. Truss was forced to resign after just 49 days in office.

The lessons of that crisis still deeply influence both British politicians and markets. According to Bloomberg, after that, pension funds were required to hold larger cash buffers and the Bank of England introduced new liquidity tools to deal with possible future market turmoil.

But the market’s alertness has not faded. Paul Markham, Investment Director at GAM Investments, told Bloomberg Radio: "There is a real memory of 1976, when the UK government was basically bankrupt. I think we shouldn’t rule out that possibility in any way."

In 1976, the UK was forced to apply for an emergency $3.9 billion loan from the International Monetary Fund.

Seven Prime Ministers in a Decade: A Governing Dilemma

The deep-rooted problems in British politics do not just stem from Starmer’s own predicament.

According to Bloomberg, the UK has now seen four prime ministers in less than four years. If Starmer steps down, the country will see its seventh prime minister in about a decade. Theresa May and Boris Johnson each served around three years, Truss lasted just 49 days, and Rishi Sunak has been in office for 20 months.

Financial Times columnist Robert Shrimsley wrote in a May 14 article that this state of affairs does not mean the UK is "ungovernable," but rather that it is "poorly governed." He pointed out that in the past decade, British politics has been full of "slogan over substance," with parties offering "fictional manifestos" during elections and avoiding real policy choices.

Starmer himself has not been exempt. Shrimsley wrote that prior to taking office, Starmer neither developed a detailed governing plan nor prepared his party for tough decisions. When welfare reform proposals reached the table, Labour MPs rebelled.

Nick Rees, Head of Macro Research at Monex Europe, said: "The market is now seriously considering the possibility that Starmer's term is ending, because there’s now a clear path for Burnham to return to Parliament."

TD Securities Head of FX Strategy Jayati Bharadwaj commented: "We expect the pound will continue to come under pressure against the dollar and euro as political friction in the UK persists."

The turbulence in UK politics is increasingly being directly transmitted to the markets. For investors, the price of this leadership changeover is already being factored in.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

IAG (Iagon) fluctuates 44.2% in 24 hours: trading volume surge triggers pump and rapid correction

British Pound hangs near one-week low vs JPY; seems vulnerable below 212.00/100-day SMA