A "welcome gift" for the new Fed Chair: Walsh has just taken office, and the market has already "raised interest rates"

Waller has not yet presided over his first Federal Reserve monetary policy meeting, but the bond market has already sent him a “rate hike present.”

On Thursday, May 14, U.S. retail sales for April posted the strongest increase in eight months, data confirming consumer resilience, but inflationary pressures continued to rise, shattering hopes of a rate cut in the short term.

After the data, the 2-year Treasury yield, which is sensitive to interest rates, climbed 4 basis points to above 4%. The 10-year Treasury yield rose to 4.48%, up about 50 basis points from its level at the end of February.

This round of repricing in the bond market is eroding the leeway that the new Federal Reserve Chair, Waller, could have had. Vincent Ahn, fixed income portfolio manager at Wisdom, said frankly, Waller originally hoped to have the option of cutting rates on his first day in office, but the bond market has already taken that option off the table.

The Bond Market Races Ahead, Yield Curve Rises Across the Board

Yields across the nearly $30 trillion U.S. Treasury market have risen comprehensively.

This week, the 30-year U.S. Treasury yield broke through the 5% mark. Although it briefly pulled back below 5% overnight, it ultimately closed at 5.030%.

Additionally, the 2-year yield climbing above the upper bound of the Federal Reserve’s short-term rate target range at 3.7% is especially notable.

Typically, the 2-year Treasury yield does not remain persistently above the federal funds target range. This abnormal pattern means that before Waller presides over his first policy meeting (scheduled for June 16 to 17), the market has already completed a round of rate tightening on its own.

Vincent Ahn described this as a textbook move by the "modern-day bond vigilantes":

They don’t destroy the Fed’s credibility with one sudden spike in yields, but rather undermine its policy options little by little by pushing the entire yield curve above the policy range.

Inflation Pressures Persist, Oil Prices Remain a Core Variable

Behind the bond market tightening are inflation signals from the real economy.

Since the outbreak of the Iran war, oil prices have surged, and the national average U.S. gasoline price has exceeded $4.50 per gallon.

Touchstone Senior Fixed Income Strategist Erik Aarts recently paid more than $6.50 per gallon to fill up in California. He stated that this is not just “very painful,” but also a daily reminder that once high oil prices persist and erode household disposable incomes, they will materially drag down consumer spending.

Many Americans have no choice but to continue to bear higher fuel costs for commuting, which means the share of wages available for other spending is shrinking. Aarts said:

The threshold for Fed rate hikes is being lowered.

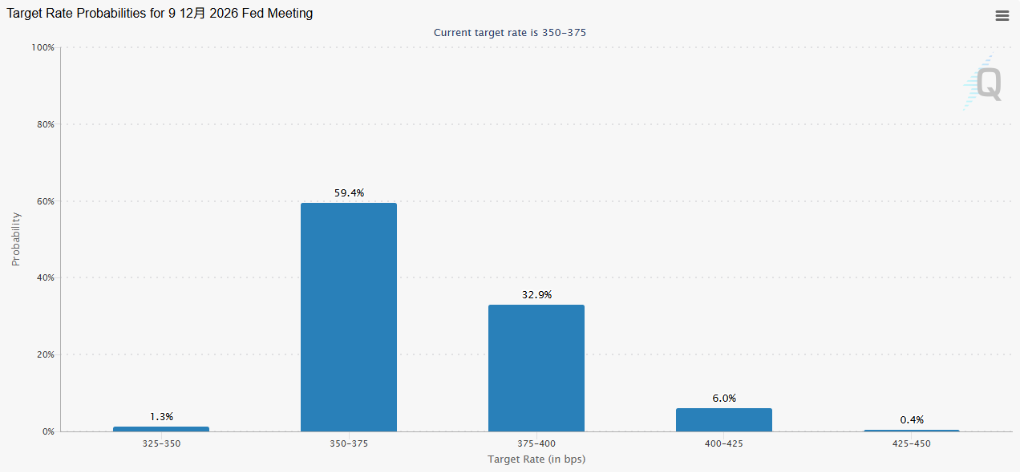

According to CME FedWatch tool, as of Thursday, the market’s expectation for a Fed rate hike before early December had climbed to over 30%, with about 60% probability of rates staying unchanged, and just a 1.3% chance of a rate cut.

Despite heightened inflation expectations, the reality of the labor market remains a constraint on the Fed’s decisions.

The April unemployment rate held at a relatively low 4.3%, but the overall job market has almost stalled. Wellington fixed income manager Brij Khurana emphasized that the Fed pays close attention to the employment market.

He points out that current inflation is fundamentally different from the wage-driven inflation of 2022, and that new employment concerns created by AI replacing white-collar positions are also brewing in the market. He said:

We’re almost watching the situation minute by minute.

In his view, as the Iran war drags on, the economic damage caused by the conflict will be more profound than the inflationary shock.

Historical Precedent: New Chair Faces Market Test

Deutsche Bank’s Jim Reid points out that it’s long been recognized that new Fed Chairs often swiftly encounter market turbulence after taking office, even as the actual data reveals a more complex picture:

- When Arthur Burns took office in February 1970, the U.S. economy was already in recession;

- Paul Volcker’s aggressive rate hikes after taking over triggered an economic contraction;

- Alan Greenspan’s era began after the October 1987 “Black Monday” crash;

- For Jerome Powell, the pandemic only hit two years into his tenure.

When Waller takes over, the stock market is at historic highs and has quickly rebounded from the early impact of the Iran war. However, the bond market’s “welcome gift” may be the truer test for the new Chair.

Jerome Powell was cautious about rate cuts as he left office under President Trump, while Waller previously argued for low rate policies in the face of high inflation.

Now, the bond market has made it clear by its actions that it does not intend to cooperate with that stance.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin Holds Above US$80,000 As Ethereum Slips Amid Fresh Crypto Volatility

Indian Rupee remains weak amid concerns over India’s forex reserves