The Real Cash Crunch and False Alarms: Why Did SOFR Surge While U.S. Stocks Didn’t Crash?【Master Cheng Tan Lecture 3.4】

Highlights Preview

Many people instinctively think when SOFR surges and repo rates spike:

“There’s a problem with dollar liquidity.”

“Are risk assets about to crash?”

But the reality might not be so simple.

In September 2019, the U.S. repo rate once soared by 300 bps;

In October 2025, SOFR once again experienced an abnormal spike.

Yet in both instances, U.S. equities didn’t see a systemic plunge,

Gold didn’t collapse; and U.S. Treasuries also didn’t suffer from broad liquidity stress.

Why?

Because a “lack of funds” in the repo market doesn’t mean the whole financial system is “short of money.”

What’s truly important isn’t SOFR itself, but whether a liquidity shock is starting to transmit to the broader financing markets.

In this lesson, Tan Cheng, founder of Tantu Macro, will systematically explain —

What a real credit crunch is;

What is just short-term disturbance caused by month-end, taxes, or debt issuance;

Why some SOFR spikes are worth caution while others are nothing to worry about;

And, above all, which liquidity indicators really determine whether risk assets are at risk.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

JPMorgan tests XRP Ledger without XRP as settlement currency

Pi Network Completes Major v23 Node Upgrade Following Complex Infrastructure Overhaul

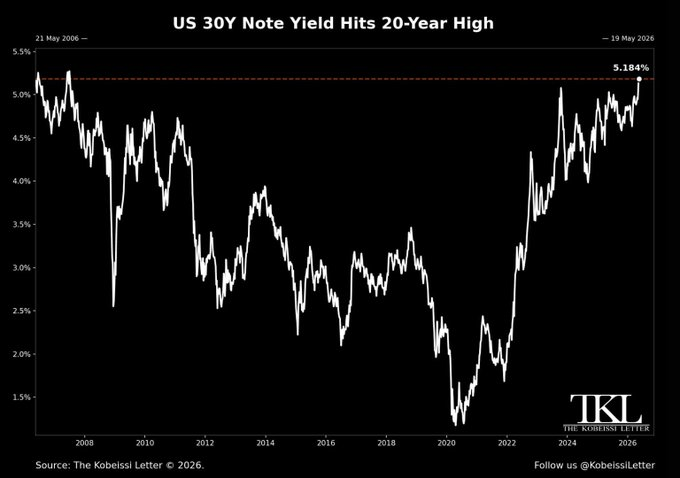

U.S. Treasury Yields Hit Multi-Year Highs as Inflation Pressure Intensifies

SHIB Burn Rate Hits 1034% Surge but Bulls Still Lose Battle at $0.0000648 Level