If the bond market turmoil continues to spread globally, what will happen next? Goldman Sachs: Nothing good

The global bond market is currently experiencing a tightening shock driven by real rates. Goldman Sachs warns that if this trend continues, risk assets, emerging markets, and even long-duration equities will face greater pressure. This is all happening against a backdrop of still-moderate inflation expectations, which leaves the market with very limited room to respond.

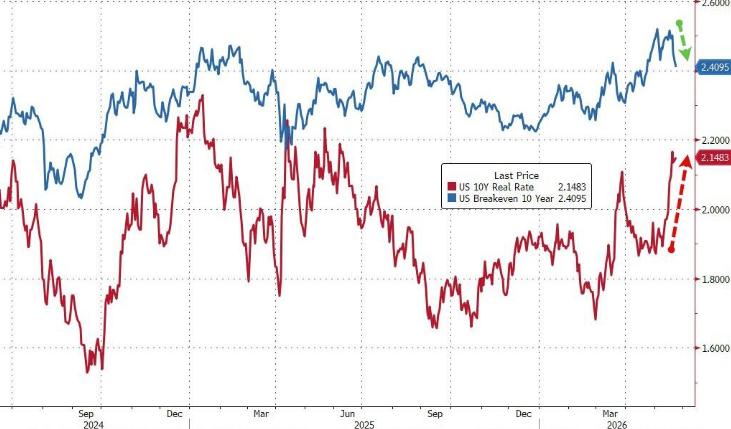

Vitali Meschoulam, Head of Global Market Strategy at Goldman Sachs, pointed out that the recent 25 basis point rise in the nominal yield on US 10-year Treasuries has been driven almost entirely by the real yield climbing to around 2.1%-2.2%, while breakeven inflation rates (breakevens) have held steady around 2.4%. This pattern has also spread to Europe and parts of emerging markets, with nominal yields rising mainly due to real rates rather than a repricing of inflation expectations.

Dom Wilson, Senior Macro Advisor at Goldman Sachs, stated during the firm’s weekend macro conference call that the 30-year US real yield is reaching historically rare highs.He warned that if the driving force behind higher real yields shifts from strong growth to concerns about fiscal sustainability or market expectations of aggressive central bank rate hikes, it would trigger a material tightening of financial conditions, and “nothing good comes from that.”

Real Rates Leading the Tightening, While Inflation Expectations Become “Accomplice”

Goldman Sachs characterizes the current macro environment as a period of “tightening without inflation” (Real Rates↑ / Breakevens→)—an institutional regime change that is clearly unfavorable for growth.

The main factors driving the rise in real rates include higher term premiums, fiscal supply pressures, and a market reassessment of the neutral real rate. Long-term inflation expectations are currently well-anchored, meaning the current inflation is of “low quality” (supply-driven), and not enough to trigger a broader reflation shift.

The dip in breakeven inflation rates last week gave the market some temporary relief. However, Goldman Sachs notes, this trend is somewhat ironic—if real rates don’t fall in tandem, lower breakevens actually reinforce the tightening shock from real rates rather than alleviate it.

Goldman Sachs believes a genuine institutional shift would require US 10-year breakeven inflation rates to clearly break above about 2.35%, a condition that has not yet been met.

Growth Narrative Supports Markets, but Vulnerabilities Are Building Up

Wilson acknowledged that the market has absorbed rising yields better than expected so far—stocks have climbed alongside yields, which Goldman’s conventional tools interpret as a significant upgrade in the growth outlook. The resilience of the US economy and labor market, as well as structural demand from AI investment, are all putting upward pressure on real rates.

“If the rise in real yields continues to be driven by strong growth and investment demand, it’s more of a brake on risk asset upside momentum than a real problem,” Wilson said, “because there’s cyclical optimism underneath.”

However, he also noted that the market’s response to rising yields is “unusually calm,” and to justify this level of absorption, a very strong growth story is needed. If that narrative shows any cracks, the market’s vulnerabilities will be revealed quickly.

If Pressure Shifts to Fiscal and Policy Concerns, Risk Assets Will Feel It First

Wilson painted a more adverse scenario: if the driving force behind rising real yields shifts from growth to fiscal sustainability concerns, or markets begin to expect aggressive central bank tightening, it would replay the market moves seen during the summer of 2023 when long-end yields surged sharply.

In that scenario, Goldman forecasts the following chain reactions:

- Spreads and carry strategies: Tighter financial conditions will directly challenge carry trades.

- Emerging markets: The emerging market assets, which are currently performing relatively well, will be subject to greater stress.

- Long-duration stocks and rate-sensitive segments: Confidence in long-duration stocks leading the market rally may be shaken, and real estate and consumer-related assets could also take a hit.

- Currencies: With global yields generally rising, currency trends become more complicated, but Wilson sees a higher probability of further US dollar strength—especially against the yen and some emerging market currencies, with potentially broader impacts.

Central Bank Response Will Determine How Pressure Is Distributed

Wilson emphasized that central bank policy response is the key variable in determining how pressures are distributed along the yield curve.

If the Federal Reserve discusses rate hikes more explicitly, it could help anchor long-end real yields—but at the cost of shifting pressure to short-end real rates and potentially driving the dollar even higher.

Conversely, if the Fed shows stronger policy restraint as concerns about the inflation and growth mix intensify, long-end pressures will continue to build, the yield curve will steepen, and long-duration as well as emerging market assets will suffer more shocks.

Wilson added that if substantial progress is made in the Iran nuclear deal negotiations, a drop in oil prices could help ease inflation expectation pressures to some extent. However, he also noted, “beyond this, it’s hard to see a path to rapid relief.”

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.