Silicon-Based Inflation and Carbon-Based Collapse: A Gray Rhino is Being Raised

01 Two Divided Worlds

The most dangerous misjudgment in the current U.S. capital market is the belief that the AI revolution brings only prosperity.

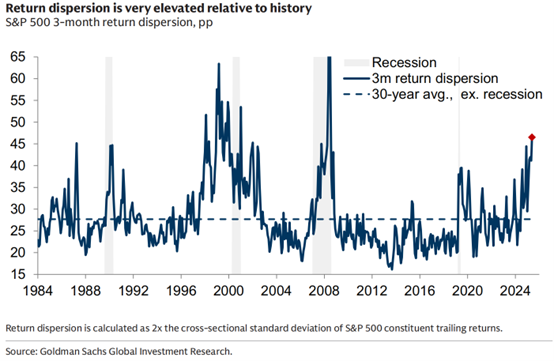

This week, Goldman Sachs raised its year-end target for the S&P 500 to 8,000 points, reasoning that 2026 and 2027 EPS forecasts have been raised to $340 and $385 respectively, with beneficiaries of the AI investment wave expected to contribute about half of the profit growth. The dispersion of market returns is at a historically high level, with a small number of winners in semiconductors, technology hardware, industry, and utilities attracting most of the capital.

(The above chart shows the S&P 500 return dispersion at a historical high, indicating a highly concentrated market rally)

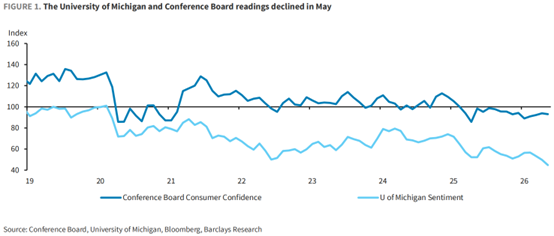

Meanwhile, U.S. consumer confidence data points in the opposite direction. The Conference Board Confidence Index fell to 93.1 in May, and the University of Michigan Index dropped to 44.8—its lowest level on record. Survey data shows that mentions of "prices, oil and gas" increased for the second consecutive month, while mentions of "war, geopolitics, and conflict" remain high.

The gap between these two sets of data is exactly the starting point of the gray rhino. This gray rhino does not suddenly charge into the trading floor one day; it is slowly being nurtured by a triple structure: AI distorts inflation signals (silicon-based inflation) → policymakers face the risk of misjudgment → real consumers (carbon-based) are having their confidence and purchasing power destroyed.

The market has only celebrated the first loop, ignoring the latter two.

02 Silicon-based Inflation: How AI Has Distorted the PCE

The first step in the formation of this gray rhino is a widely overlooked technical issue: AI is distorting the core indicators used to measure inflation in the U.S. in a counter-intuitive way.

According to recent research by soon-to-depart Fed Governor Miran and collaborators, due to statistical differences, AI-related prices—especially computer flash memory—carry a weight in the core PCE that is about forty times that in the CPI. In recent months, core goods CPI has seen almost zero growth, but core goods PCE has recorded a month-on-month increase of 0.3%. Miran and others conclude: the PCE "inappropriately overweights these prices," effectively using computer storage prices to deflate a much larger category of consumption that should not be tied to it.

……

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trending news

MoreTrump's remark ignites global markets! Markets bet on Middle East ceasefire: oil prices plunge 17% in May, US stocks reach new highs, Bitcoin surges past $74,000, US dollar falls below 99

Gold launches a sudden counterattack! Trump releases major Middle East positive news, gold surges $100 to approach $4600