The 'bull market' confidence: Global corporate earnings have 'decoupled from fundamentals', profit margins set to hit record highs, and 'AI impact similar to China joining the WTO'

Global stock markets continue to reach new record highs, but the core logic supporting this bull run has diverged from traditional macro fundamentals in an unprecedented way. In its latest report, Bank of America Securities warns that the market is pricing in a structural leap in corporate profit margins driven by the AI revolution as an almost certain base scenario. Whether these expectations can come true still depends on several stringent conditions being met simultaneously.

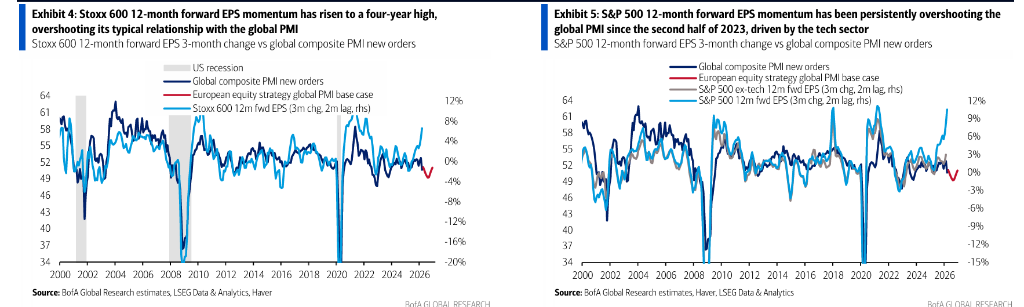

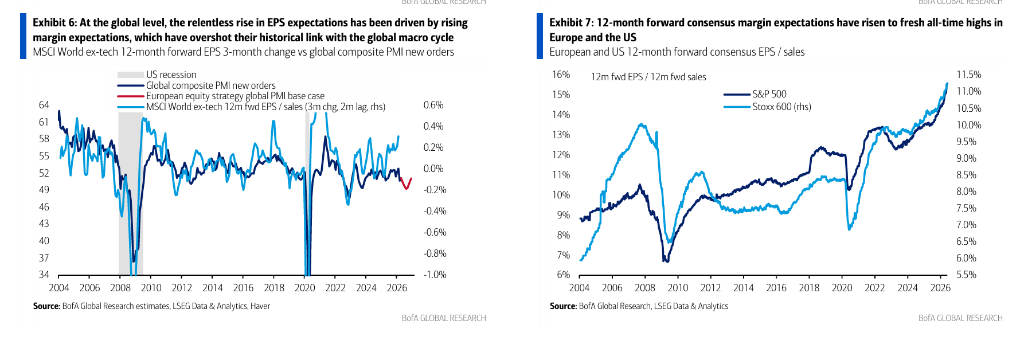

The MSCI Global Index’s 12-month forward Earnings Per Share (EPS) has risen 9% over the past three months, an annualized gain of nearly 40%—the strongest since 2021; the S&P 500 Index’s three-month EPS momentum has reached 12%, a 40-year high. Historically, such levels have only occurred during strong recoveries from recessions. The anomaly in this round of strong earnings is that the global PMI has fallen to a two-year low of around 50.5, which, following historical patterns, should point to flat or even lower EPS expectations. Bank of America data shows that in the past three months, about two-thirds of EPS upgrades in Europe and globally were due to higher margin expectations. Both European and global 12-month forward consensus profit margins have hit all-time highs, at 13.9% and 11.4% respectively.

According to Chasewind Trading Desk, Bank of America Securities’ strategy team likens this phenomenon to the historical impact of China’s accession to the WTO in 2001 on corporate profitability. At the time, over one billion Chinese workers entered the global market, significantly weakening the bargaining power of developed countries’ workers, pushing the share of post-tax corporate profits in GDP from 5-8% to 10-12%, where it remained at elevated levels thereafter. Now, the large-scale deployment of AI tools could similarly erode the bargaining power of white-collar workers, enabling companies to use lower-cost AI to replace labor and further capture a larger share of national income.

However, Bank of America Securities remains cautious about this narrative and maintains a negative rating on European equities. The institution argues that the market currently takes the “no demand concerns, record earnings” ideal scenario as baseline, while in reality, multiple downside risks are being systematically underestimated and upside risks are already overly priced in.

Earnings Expectations Hit Record Highs, "Decoupled" from Macro Indicators

Global stock markets hit fresh record highs again this week, with year-to-date gains expanding to 9%. According to Bank of America Securities’ European equities strategy report from May 29, this surge is jointly driven by three major factors: expectations of US-Iran peace pushing Brent crude down to a one-month low of $93 per barrel, continued resilience in global macro data, and a significant leap in corporate earnings forecasts.

For the year to date, 12-month forward EPS expectations for Europe, the US, and the world rose by 8%, 15%, and 11% respectively, while stock prices in the same periods rose by 6%, 10%, and 9%. This means this year’s stock market gains have been fully supported by earnings growth, with valuation multiples actually declining slightly.

However, there is a notable anomaly in this round of EPS growth: historically, EPS momentum has been highly correlated with the Global Composite PMI New Orders Index, but now the global PMI continues to fall to a two-year low of around 50.5. According to past experience, this should result in flat or lowered EPS expectations, but the market is moving against this trend. In Europe, where earnings typically lag, 12-month forward EPS rose 7% over three months, also the strongest since 2021.

More importantly, the core driver of this EPS upgrade cycle is the expansion of margin expectations, rather than sales growth. Since 2022, margin expectations have consistently surpassed levels implied by global macro cycles, and the extent of this overshoot has widened further. Currently, the 12-month forward consensus profit margin in Europe is 13.9% and globally is 11.4%, both all-time highs. Meanwhile, the three-year forward annualized EPS growth rate has climbed to a five-year high of 16%, showing that market consensus firmly believes current high profit margins will persist.

"AI Effect Similar to China’s WTO Entry": Market Bets on Structural Leap in Profit Margins

To explain this anomaly, Bank of America Securities strategists offer a historically informed analytical framework. The report highlights that the start of margin expectations exceeding macro logic closely coincides with the launch of ChatGPT at the end of 2022. The most convincing explanation is that the market is pricing in a structural boost to corporate profitability driven by the AI revolution.

The historical precedent for this logic is China’s WTO accession in 2001. China’s entry brought over a billion workers into the global economy, sharply lowering the bargaining power of workers in developed countries. This shifted US non-financial corporate labor compensation as a share of GDP from its decades-long range of 61-65% down to 57-60%; at the same time, post-tax corporate profits as a share of GDP jumped from 5-8% to 10-12%, staying at the higher level thereafter.

The report argues that the large-scale deployment of AI tools could have a similar effect on white-collar workers—as external competition at the turn of the century reshaped the blue-collar labor market, AI competition may further erode white-collar bargaining power, allowing companies to replace human capital with cheaper AI. This would enable another structural uplift in profit margins without a macroeconomic acceleration.

On the valuation side, this logic is also corroborated by market signals: the ratio of US stock market capitalization to GDP recently hit an all-time high of 225%, and the global market capitalization to GDP ratio reached 105% for the first time. Bank of America believes that if companies truly capture a larger share of the economy, the intrinsic value of equity as an asset class should rise proportionally to the overall economy.

It is important to emphasize that this is not simply a tech sector phenomenon. Excluding tech stocks, the MSCI Global Index’s 12-month forward consensus profit margin also rose to a record 12%, while tech stocks are expected to contribute 23% of global corporate earnings in the next 12 months—a record high.

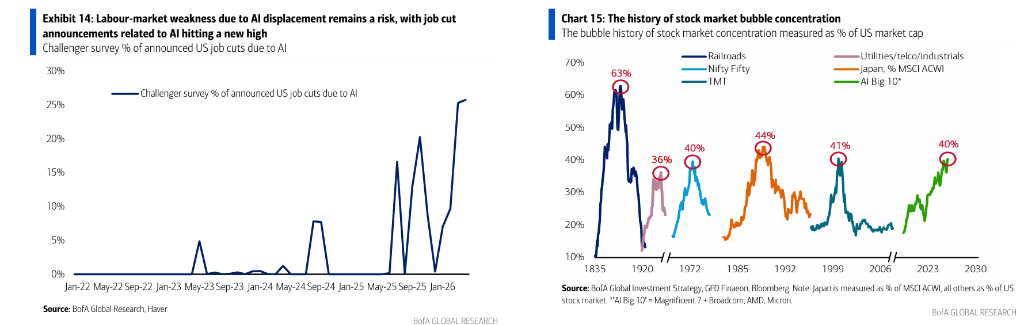

Of course, Bank of America also points to an alternative interpretation: historically, at the start of each wave of large-scale corporate investment booms, profit margins briefly inflated due to capacity scarcity and robust demand. However, as depreciation and supply expanded, margins later contracted. This "boom-bubble-bust" pattern was seen in the railway craze of the 1880s, the radio boom of the 1920s, and the tech boom of the 1990s.

Five Major Barriers: Risks on the Path to a "Golden Age of Corporate Profits"

Bank of America Securities stresses that the vision of a "golden age of corporate profits" is not logically impossible, but for the ideal scenario to become reality, a host of conditions must materialize simultaneously. At present, at least five major potential barriers remain:

First is exogenous macro downside risk. EPS momentum has already exceeded PMI-implied historical levels but is unlikely to totally decouple from fundamentals. Global oil inventories are tight, and the Brookings Institution estimates that if energy flows through the Strait of Hormuz are not restored in time, a new supply-demand balance would have to be achieved through demand destruction. Prediction markets currently assign only about a 34% chance of the Strait returning to normal by early July, and around a 55% chance by early August. Meanwhile, Bank of America economists note that US real disposable income growth has fallen to recessionary levels, and prior fiscal stimulus supporting consumption is being depleted.

Second is endogenous macro downside risk. The core premise of the AI-labor substitution narrative is that companies replace labor with AI, but if multiple firms downsize simultaneously, it could further weaken an already fragile labor market, leading to the "Paradox of Thrift" described by Keynes. Bank of America data shows the three-month non-farm payroll growth in the US is still near zero—a level historically highly correlated with recessions. The report also notes that the proportion of layoff announcements related to AI has recently hit a new high.

Third is rising AI usage costs. According to Bloomberg data (Silicon Data LLM Token Expenditure Index, SDLLMTK), token usage costs for large AI models have doubled since the start of the year, due to factors like pre-IPO subsidy cuts by AI model providers, a surge in agentic AI raising token usage, and higher energy costs. Bank of America has observed some companies cutting back on AI usage due to rising costs; if this trend continues, it would undermine the core assumption of AI’s economic advantage over labor.

Fourth is uncertainty around the timeline for productivity gains. The market is currently pricing in immediate returns of AI to corporate productivity, but Bank of America economists estimate—based on bottom-up data—that AI’s current annual contribution to productivity growth is only about 0.1 percentage points, and its full impact may take a decade to materialize, creating a significant gap from market expectations for instant profit jumps.

Fifth is political risk. Even if mass AI substitution of white-collar workers does not trigger significant labor market shocks, it could spark larger political backlash—raising pressure for windfall taxes on successful tech companies, just as the loss of blue-collar jobs previously fueled the populist waves of the 2010s and 2020s. The report cites recent calls in South Korea for a "national dividend" funded by AI profits as an early signal of such political pressures.

Bank of America Maintains Negative Rating on European Stocks, Recommends Underweighting Cyclicals

Based on the above comprehensive judgment, Bank of America Securities maintains a negative overall rating for European equities and expects about 10% downside potential for the Stoxx 600 Index by the end of Q3, targeting 560 points, and 590 by year-end.

Bank of America’s core argument is that the market is currently overestimating the probability that AI-driven structural margin upgrades will be realized, while underestimating the risk of demand destruction from energy shocks. The Stoxx 600’s equity risk premium (ERP) is currently 4.6%, only 10 basis points above the 20-year low set earlier this year. Market pricing implies that global PMI will rise moderately, which diverges from BofA’s macro team's forecast.

In terms of sector strategy, Bank of America is overweight in defensive sectors such as food & beverage and pharmaceuticals, as well as quality stocks; underweight in banks and capital goods, and maintains a negative view on relative performance of cyclicals versus defensives. This ratio is now at a 30-year high, and BofA expects about 10% downside risk.

Bank of America notes that if the expected macro downturn and increased risk premiums materialize, this year’s earnings-driven story will be put to the test—a scenario where profit margin expectations are downgraded and valuation multiples contract simultaneously. Of course, the institution also acknowledges that if the scenario the market expects does come true—rapid arrival of AI-driven efficiency dividends, ongoing macro resilience, and an energy crisis resolution—then the current high margin expectations may be validated. However, BofA believes that this nearly ideal scenario has already been priced in with excessive certainty.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Data security in AI jumps 10 as privacy risks surge

Hackers drain $5.4M from Gravity’s Ethereum – Cosmos bridge

Bitcoin 200 week moving average passes $61,000 mark

Dogecoin struggles to hold $0.10 as risks remain high