Beyond Trade Settlement: The Internationalization of the RMB Ushers in a Golden Window

Recently, the internationalization of the RMB has clearly accelerated, but unlike in the past, the core driver of this round of expansion is no longer just trade settlement. It has now begun extending to cross-border investment and financing, offshore asset allocation, and global financial infrastructure.

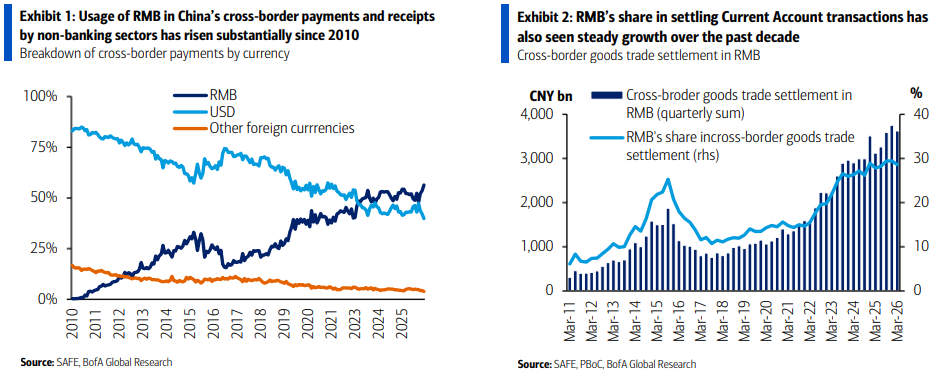

First, in terms of cross-border payments and settlement, RMB usage has surged dramatically. The proportion of RMB used by non-bank sectors in China’s cross-border receipts and payments has skyrocketed from 17% at the end of 2016 to 56% in March of this year—more than doubling—and has effectively reversed the previous absolute dominance of the US dollar (meanwhile, the dollar’s share fell to 40% over the same period). At the same time, the Cross-border Interbank Payment System (CIPS) has seen explosive growth in activity, with average daily transaction volumes jumping nearly 50%. On a single day in April this year, transaction volume hit 1.22 trillion RMB, marking a historic high.

Second, the foundation of commodity trade settlement has become increasingly solid. In March and April 2026, the proportion of commodity trade settled in RMB reached a historic high of 33.5%, a significant jump from the average of 11.5% between the end of 2017 and 2022.

Additionally, the offshore financing market has entered a boom period. Against the backdrop of high global interest rates and an inverted Sino-US interest rate spread, the market for Chinese USD bonds continues to shrink, while the offshore RMB bond (“Dim Sum bond”) market has instead expanded by more than two times, reaching a total size of $244 billion. Since the beginning of this year, issuances by foreign entities (especially global banks) have increased by 180% year-on-year, accounting for half of all offshore RMB bond issuances.

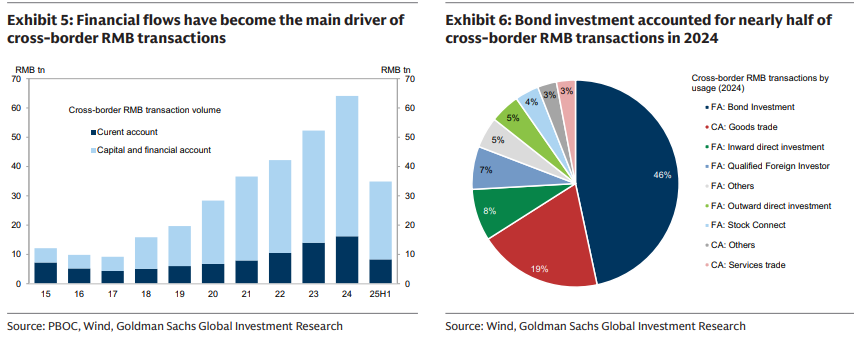

More importantly, the structure of cross-border RMB usage has changed significantly. Previously, RMB internationalization mainly relied on the current account and trade settlement; now, capital and financial account transactions make up 75% of the total. Among these, bond investment accounts for 46% and has become the largest single use of cross-border RMB payments, far surpassing commodity trade (19%). This means that the next stage of RMB internationalization will no longer just depend on trade settlement and pricing, but will rely more heavily on the attractiveness and liquidity of RMB financial assets.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US strikes Iranian targets as peace deal remains elusive, crypto markets reel

How far has the AI "bubble" progressed?

Micron Stock Forecast: Can MU Sustain Its AI-Driven Breakout After Record High?