跑贏華爾街所有目標價!「AI大牛股」Palantir的高增長故事還能怎麼講?

Jefferies 分析師Brent Thill寫道:“雖然基本面良好,但 Palantir 必須連續四年將銷售額增速提高到 40%,市盈率達到 2028 年預計收入的 12 倍,才能維持股價。”他還表示,這“似乎不太可能”。根據彭博社彙編的數據,市場普遍預期今年該公司的增長率為 26%,明年為 24%。Thill 將該股評級下調至“表現不佳”,理由是其估值不可持續。

Jefferies 分析師Brent Thill寫道:“雖然基本面良好,但 Palantir 必須連續四年將銷售額增速提高到 40%,市盈率達到 2028 年預計收入的 12 倍,才能維持股價。”他還表示,這“似乎不太可能”。根據彭博社彙編的數據,市場普遍預期今年該公司的增長率為 26%,明年為 24%。Thill 將該股評級下調至“表現不佳”,理由是其估值不可持續。 Zhito Finances APP noticed, $Palantir (PLTR.US)$ The performance has left skeptics puzzled, although some Wall Street analysts question its high valuation and the sustainability of the company's revenue growth, its stock price continues to rise.

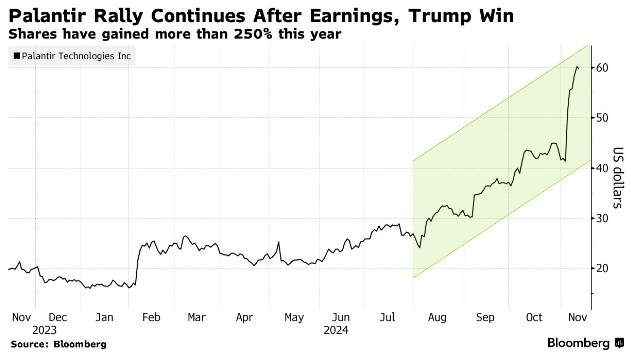

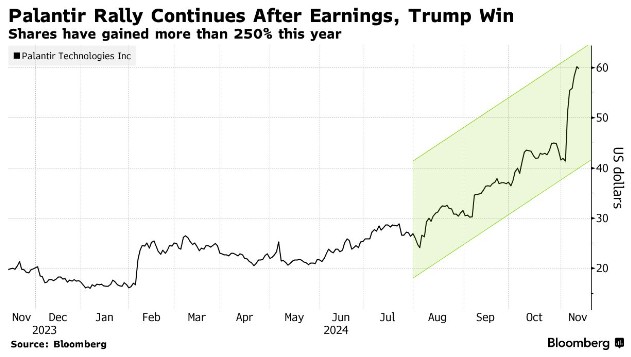

Palantir has risen by more than 250% this year, with a large part of the increase coming from last week's better-than-expected earnings. Trump's election victory has also added momentum to the company, with bulls pointing out the company's relationship with Trump's administration and the potential for the new government to promote ai to boost sales.

The recent rally has further pushed up Palantir's already high valuation. The company's expected pe ratio is about 135 times, significantly higher than the average pe ratio of about 27 times for companies in the Nasdaq 100 index. In terms of enterprise value to revenue ratio, it is also the most expensive stock in the S&P 500 index. For some investors, its surge has been too much, with two analysts downgrading the stock rating in the past week.

Jefferies analyst Brent Thill wrote: "Although the fundamentals are good, Palantir must increase its sales growth rate to 40% for four consecutive years and achieve a pe ratio of 12 times the expected revenue in 2028 to sustain its stock price." He also stated that this "seems unlikely". According to data compiled by Bloomberg, the market generally expects the company's growth rate to be 26% this year and 24% next year. Thill downgraded the stock rating to "underperform" citing its unsustainable valuation.

Jefferies analyst Brent Thill wrote: "Although the fundamentals are good, Palantir must increase its sales growth rate to 40% for four consecutive years and achieve a pe ratio of 12 times the expected revenue in 2028 to sustain its stock price." He also stated that this "seems unlikely". According to data compiled by Bloomberg, the market generally expects the company's growth rate to be 26% this year and 24% next year. Thill downgraded the stock rating to "underperform" citing its unsustainable valuation.

Argus Research analyst Joseph Bonner expressed a similar view. Bonner wrote: "Palantir's stock price has already doubled this year, possibly exceeding what the company's fundamentals can support." He downgraded the stock to hold.

He added: "Palantir caters to a small fraction of organizations facing highly complex IT challenges, which could lead to unbalanced outcomes, and the market tends to penalize technology stocks with high valuations."

Wall Street's conflicting attitude towards the stock is reflected in the analyst data tracked by Bloomberg. Among the 20 companies researching the company, half give a 'hold' or equivalent rating, while three companies rate Palantir as a 'buy' and seven companies recommend 'sell'. The average target price implies a 39% decrease - a significant gap from the current trading, which may also be partially attributed to Palantir's group of retail investors, who are one of its biggest supporters.

There are other signs that some people believe this rally has gone too far. According to data from S3 Partners LLC, with Palantir's stock price soaring, short sellers betting against Palantir have incurred over $3.6 billion in losses this year. However, they are doubling down on the stock falling, as data shows that the short interest in Palantir has risen from 2.8% in early September to 4.6% this week.

On the other hand, Trump's decisive election victory has given bulls a new reason to be optimistic about the company, as over half of the company's revenue comes from government contracts.

DA Davidson's Gil Luria gives the stock a 'neutral' rating, believing that Palantir will benefit from its close ties with Trump, as CEO and co-founder Alex Karp, co-founder Joe Lonsdale, and chairman Peter Thiel 'all have very close ties to this administration'.

Luria stated in an interview that Palantir's vision 'aligns with Trump and his government's ideology', especially in the 'clear vision of selling only to Western countries', and added that the company is 'a standard-bearer for patriotic American companies'.

Wade Bush Securities analyst Dan Ives is a long-term bull on Palantir. He believes that with the new government's strong push for artificial intelligence, the company will be able to win more government contracts. He wrote: 'We expect significant AI programs within the U.S. government, including the Department of Defense, to be a major positive.'

Despite this, even Ives's highest Wall Street target price of $57 has been surpassed in the past week, highlighting the speed and extent of Palantir's latest rally, and the challenge investors face when reaching the top.

Editor/ping

免責聲明:文章中的所有內容僅代表作者的觀點,與本平台無關。用戶不應以本文作為投資決策的參考。

您也可能喜歡

美聯儲放了那麼多水,為什麼市場還會缺錢?【程坦大師課3.5】

「以價換量」告一段落?特海國際第一季度利潤率修復

SpaceX IPO:史上最大上市,2萬億美元的定價難題

英特爾CEO陳立武鐵腕新規:若芯片兩次流片未能量產,員工將被炒魷魚